We can save ourselves from the tax trap by investing in various tax saving schemes. Normally people have the tendency to do their tax planning when they near the end of the year, but we should start our tax planning before the financial year nears its end.

| Table of Contents |

|---|

| Best Tax Saving Schemes |

| How much total tax can one enjoy in Individual File? |

| Bottomline |

Thus in order to avoid making unnecessary investments, due to absence of time for planning, we should plan well ahead and research properly before filing for our returns thus making our tax plan investments useful for us

It is always good to start investing in the early quarters of the financial year. Learning the science of wealth management or financial planning can make you an expert in striking a balance between tax saving, return and risk.

It will require some dedicated work from your end, but as they say nothing comes without efforts.

Learn in detail about various taxes with Insurance and Taxation Made Easy course by Market Experts

Now let’s delve into various tax saving schemes-

Best Tax Saving Schemes

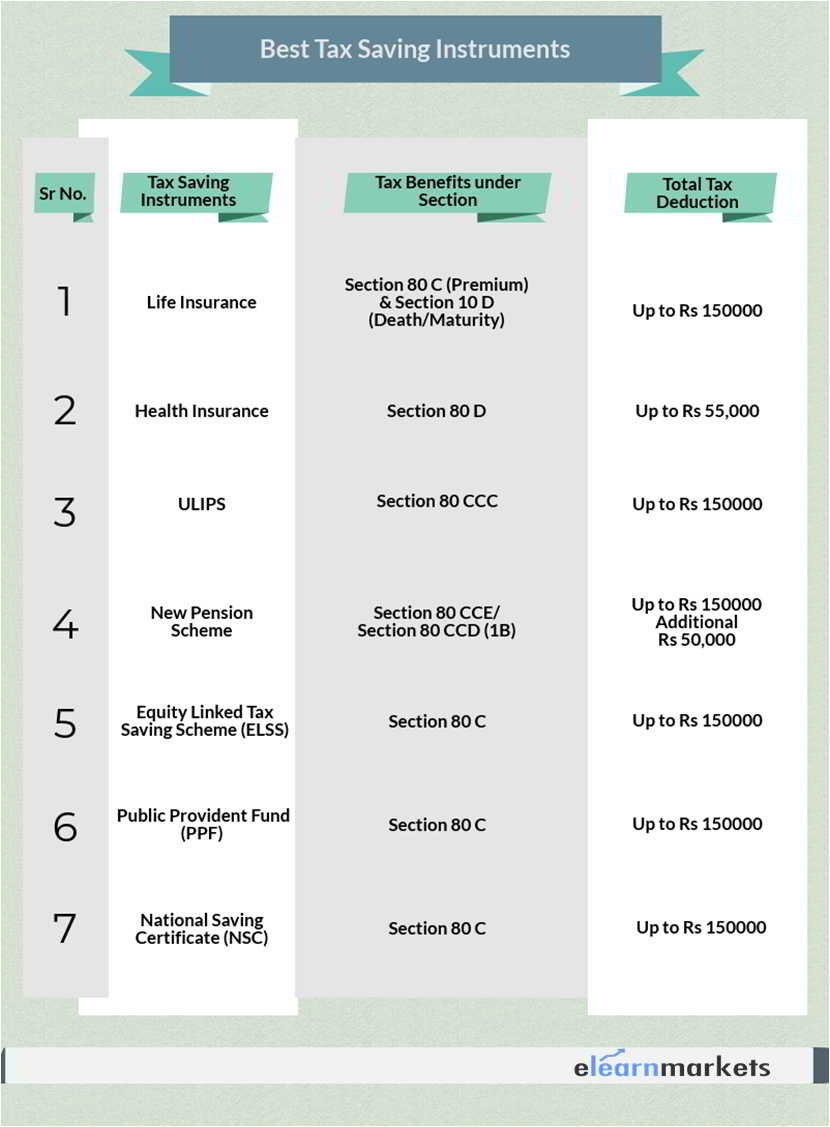

Life Insurance

Every income tax payer should have life insurance policy not only for tax exemption but also to secure his/her family.According to 2018-2019 budget, life insurance offers tax benefit of up to Rs 1.5 lakh under section 80 C of the Income Tax Act as shown in the table above. It is one of the best tax saving instruments. Also in the case of death, the lump sum amount which is offered to the beneficiary is not taxable under section 10(10D).

Health Insurance

Health insurance or Mediclaim is one of the tax saving instruments and policy that every family should possess to protect against any illness. Under mediclaim, tax deductions are availed on the premium paid under section 80D. Thus premiums up to Rs. 25,000 are subjected to tax deductions. If we purchase health insurance for ourselves as well as our parents, then we are eligible for deductions up to Rs. 50,000.

Unit Linked Insurance Plan (ULIPs):

For a long term investment, Unit Linked Insurance Plan is one of the good tax saving instruments. The premiums are invested in debt and equity. It also offers insurance to our investment. We can expect good returns if we invest in it for 10-12 years. In the case of ULIPs, there is no premium holiday. Your policy can get discontinued if youe fail to pay the premium. It is the only tax saving instrument which allows us to switch from equity to debt. It allows tax deduction of up to Rs. 1.5 lakh under the section 80 CCC of the Income Tax Act.

New Pension Scheme (NPS)

If we are looking for a tax saving instrument which offers both retirement and tax benefits, then the New pension Scheme is the best investment option. It is a low cost and friendly investment option. We can invest a minimum amount of Rs. 6000 in instalments as well as lump sum. An investor can also choose where to allocate money, whether in equity, gilts or corporate bonds.

Equity Linked Tax Saving Scheme (ELSS)

Equity Linked Tax Saving Scheme (ELSS) is a short term investment option with a lock in period of 3 years. The minimum amount which can be invested is Rs. 500. As it invests in equity, ELSS is a good tax saving instrument for even long term. We are not bound to continue after the lock in period gets over. It is always better to invest our money over a period of time than investing in lump sum. One can get a tax deduction of Rs. 1.5 lakh under section 80 C of the Income Tax Act.

Public Provident Fund (PPF)

This is one of the most preferred long term tax saving investment options under section 80 C of the Income Tax Act. It has a lock- in period of 15 years and can be extended in blocks of 5 years. According to the 2018-2019 budget, the investment limit has been extended from RS. 1 lakh to Rs. 1.5 lakh. The minimum amount that can be invested in Public Provident Fund (PPF) is Rs. 500 and the maximum amount that can be invested is Rs 1.5 lakh. It is one of the best tax saving investment for the people who are not covered under Employee Provident Fund like the self employed professionals.

National Saving Certificate (NSC)

It is a fixed deposit service which is offered by the post office. As National Saving Certificate (NSC) is different from a bank fixed deposit, it offers fewer returns. But this investment scheme is Government secured. Therefore our money is completely safe. It has a lock in period which ranges from 5 years to 10 years. The longer we invest in NSC, the more we will become eligible for extra tax deductions.

Watch the video below to know more about 7 best tax saving schemes :

How much total tax can one enjoy in an Individual File?

Investment Deductions

Section 80CCC applies to Annuity Plan for oneself or bonus received on it or from it.

Under Section 80CCD one can take benefits of EPPF which is 10% of salary or 20% of gross Income or Rs1,50,000 whichever is less.

Section 80CCD(1B) allows additional deduction of 50,000 under National Pension Scheme( NPS) account or Atal Pension Bima Yojana

Section 80CCD(2) allows Employers to contribute for the employees’ pension upto 10% of his/her salary. There is no monetary ceiling on this deduction.

Thus an individual can save total tax worth 1,50,000 under 80C in heads like ELSS + Mediclaim + HRA + LIC + PPF + Tuition Fees = 1,50,000

Bank Interest Deductions

Section 80TTA(1) allows a person to claim deduction upto 10,000 against interest received by bank or post office or cooperative society. It excludes interest received on FD, Recurring Deposits or Corporate Bonds.

Section 80 TTB allows senior citizens to save on Interest from banks, Post Office etc upto a maximum of 50,000

Thus an individual can save total tax worth 10,000-50,000 depending on his/her age

House Rent Allowance (HRA)

Section 80GG allows deduction for house rent paid if House Rent Allowance is not received from the employer upto a maximum of 60,000 per year or 25% of total Income.

Thus an individual can save total tax worth 60,000 or 25% of total Income.

Education Loan

Section 80E exempts interest on Education Loan taken, for 8 years.

Section 80EE exempts first time home loan takers upto Rs50,000

Thus an Individual can save upto Rs 50,000 or Interest paid for 8 years

Mediclaim

Under Section 80D one can take exemption for Mediclaim worth Rs25000 below the age of 60 Rs50,000 for people above the age of 60

Section 80DD exempts for Medical for handicapped from Rs75000-Rs125000 depending upon the severity of handicap.

Under Section 80DDB one can claim exemptions for medical expenses incurred for diseases specified under 11DD worth 40000 for people below 60years of age and 100000 for people above 60years of age

Under Section 80U a person suffering for mental or physical disability can claim deduction for self worth Rs 75000-Rs125000

Thus an Individual can save between Rs25,000-Rs1,25,000 depending on the criteria

Donations

80GGB exempts contributions from companies to political parties which remains infinity if paid in cheque but can’t be claimed if paid in cash.

80GGC exempts contributions from individuals to political parties which remains infinity if paid in cheque but can’t be claimed if paid in cash.

80RRB exempts income by way of royalty on patent till Rs3,00,000

Bottomline

We should plan our savings not only for tax exemptions but also for a better and financially stable future. We should save our hard earned money from getting depleted by paying taxes on it. The above investment options can help us to achieve the targets of tax saving and also provide good returns for our Future needs.

{kind=link}

Great article, Great content with all the helpful information.Thanks for sharing!

I found your article very informative and useful. Thanks for sharing!

Hi,

Thank you for reading our blog!

Keep Reading!!