Basics Of Options

Introduction

In this module, we will dive into the complexities of options. We will decode all the concepts related to options. Unlike futures contracts, an option contract offers us the choice of whether to exercise the contract or not. It is an extremely beneficial instrument among traders in the market. We will not only cover the basic concepts but also learn the different types of options available to trade in the market. We will also be discussing how options contracts are priced and the factors that affect the options premium. This module is a complete package where you can gain immense knowledge of options and develop skills related to option trading.

So, without any further ado, let's get started:

Understand Options

What are option contracts?

In futures contracts, theoretically there is a possibility of unlimited profit and unlimited loss. If you trade in Futures contract, you have an obligation to bear that loss or gain profits as the case may be, depending on the spot price on expiry.

If you enter into a contract to buy or sell an asset at a particular price, on expiry you have the obligation to fulfil it, irrespective of the current market price. Right?

Now what happens if you have a choice? Or right? If a derivative contract can give you choice or right, a right to enter into the contract or simply back out at a later stage. What if you don’t have an obligation to fulfil the contract?

Do you think the choice or right is available? The answer is YES!

This choice is called OPTION, a type of derivative contract that gives you a CHOICE.

Choice to buy or sell. Choice between Right and Obligation.

- When you chose right – you are the buyer of that choice

- When you choose an obligation – you are the seller of that choice.

- When your choice is to buy – it is called a call option

- When your choice is to sell – it is called a put option.

Let me decode this for you with the help of an example.

Assume Saksham is bullish on a stock. It is trading at ₹670/- today. He has the right today to buy the same stock one month later, at say ₹ 750/-.

Now If the share price on that day is more than ₹750? He would buy it. It means that after 1 month even if the share is trading at ₹850, Saksham can still get to buy it at ₹750! In order to get this right, he is required to pay a small amount today, say ₹50/-.

If the stock price moves above ₹750, he can exercise his right and buy the shares at ₹750/-. If the share price stays at or below ₹750/- he does not exercise his right and he does not need to buy the shares.

Saksham has to lose ₹50/- in this case. An arrangement of this sort is an Option Contract.

After Saksham gets into this agreement, there are only three possibilities which can occur.

1. The stock price can increase, - say ₹850/-

2. The stock price can fall - say ₹650/-

3. The stock price can remain same at ₹750/-

Case 1: If the stock price goes up, then it would make sense in exercising his right to buy the stock at ₹750/-.

The profit and loss would look like this –

Price at which stock is bought = ₹750

Premium paid = ₹50

So total Expense incurred = ₹800

Current Market Price = ₹850

Profit = 850 – 800 = ₹50/-

Case 2 – If the stock price goes down to say ₹650/- obviously it does not make sense to buy it at ₹750/- as effectively he would be spending ₹800/- (750+50) for a stock that’s available at ₹650/- in the open market.

In this case, he will incur a loss of ₹50 only (premium paid).

Case 3 – Likewise if the stock stays flat at ₹750/- it simply means he is spending ₹800/- to buy a stock which is available at ₹750/-, hence he would not invoke his right to buy the stock at ₹750/.

In this case, he will incur a loss of ₹50 only (premium paid).

Let us dig more into this example and answer a few questions with logic.

Why did Saksham enter into this contract even though he knows that he might lose ₹50 if the stock price does not increase or stay flat?

- Saksham would lose ₹50, but the best part is that he knows that, this is his maximum loss before hand. Hence there are no negative surprises for him. Also, as and when the stock prices increase, so would his profits.

- Under what circumstances does Saksham's trade make sense? - Only when the price of the stock increases.

- Under what circumstances would the seller of the contract’s position make sense - Only that scenario when the price of the stock decreases or stays flat.

So Why do you think the other party or the seller is taking such a big risk? He would lose a lot of money if the stock prices increase after one month.

Well, think about it. There are only three possible scenarios, out of which two benefit the seller.

Statistically, the seller has 66.66% chances of winning the bet as opposed to Saksham’s 33.33% chance.

Let us summarize a few important points now –

- The payment from Saksham to Seller ensures that Saksham has a right (remember only he can call off the deal) and Seller has an obligation (if the situation demands, he has to honour Saksham’s claim). Saksham is an option buyer and Seller of the contract is the option seller.

- The outcome of the agreement at termination (end of 1 month) is determined by the price of the stock. Without the stock, the agreement has no value. The Stock is therefore called an underlying and the agreement is called a derivative. An agreement of this sort is called an “Options Agreement”

- The agreement is entered after the exchange of ₹50, and this is the price of this option agreement. This is also called the “Premium” amount.

- Every variable in the agreement –Stock, Price and the date of Execution is fixed.

- As a thumb rule, in an options agreement the buyer always has a right and the seller has an obligation.

What is long on option?

Buyer of an option is said to be “long on option”. As we have discussed earlier, he/she would have a right and no obligation with regard to buying/ selling the underlying asset in the contract. So basically, when you are long on equity option contract:

- You have the right to exercise that option.

- Your potential loss is limited to the premium amount you paid for buying the option.

- Profit would depend on the level of underlying asset price at the time of exercise/expiry of the contract.

What is short on option?

Seller of an option is said to be “short on option”, he/she would have obligation but no right with regard to selling/buying the underlying asset in the contract. When you are short (i.e., the writer of) an equity option contract:

- You have the obligation to fulfil the contract.

- Your loss is not limited. It depends on the price of the underlying asset.

- Your maximum profit is limited to the premium received.

Option Terminology

Now, let us discuss the various terms associated with the options contracts.

Option Contract:

An option contract is an agreement between two parties to buy/sell an asset (stock or futures contract as an example) at a fixed price and fixed date in the future.

Underlying Asset

The underlying asset is a specific asset on which an option contract is based. The contract value is determined by the value of the underlying – so in our example the underlying asset is the stock.

Strike /Exercise Price

The specific asset price at which the asset can be bought or sold when the contract is exercised is called Strike Price i.e., ₹750/- in this case.

Expiration Date

The last day an option exists. It is generally the last Thursday of the month in case of stocks.

Options Premium

The amount per share that an option buyer pays to the seller is called option premium – ₹50/- in our example.

Option Buyer

The buyer of the option gains the right, but not the obligation, to engage in some specific transaction on the asset. In our example- Saksham is the buyer of the option.

Option Seller

The seller incurs the obligation to fulfill the transaction if so requested by the buyer.

Buyers and Writers

The people who buy the options are called ‘buyers’ or ‘holders’, and those who sell the options are called ‘sellers’ or ‘writers'. Buyers are said to have ‘long’ positions and sellers are said to have ‘short’ positions.

American Vs European Options

In this section, let us discuss the two common types of Options: American and European Options.

Initially when option was introduced in India, there were two types of options available – European and American Options. All index options (Nifty, Bank Nifty options) were European in nature and the stock options were American in nature.

The difference between the two was mainly in terms of ‘Options exercise’.

European Options – If the option type is European then it means that the option buyer will have to mandatory wait till the expiry date to exercise his right. The settlement is based on the value of the spot market on expiry day.

American Options – In an American Option, the option buyer can exercise his right to buy the option whenever he deems appropriate during the tenure of the options expiry. The settlement depends on the spot market at that given moment and not really depended on expiry.

Introduction to Call Options

Earlier, we have learned that there are two different types of options contracts: Call option and Put option. So first, let us understand: What are Call options?

An option that conveys the right to buy something is called a call option.

It gives the option to buy a stock at a certain predetermined price, so the buyer would want the stock to go up. The call option buyer believes that the underlying stock will rise because if this happens, the buyer will be able to acquire the stock for a lower price and then sell it for a profit.

A call option writer believes that the underlying stock's price will drop relative to the option's strike price during the life of the option. That is how he or she can reap maximum profit.

A long call is simply the purchase of a call option. It is a Bullish Strategy.

When to use it?

When we expect the spot price to be more than the strike price, and we are bullish on market direction.

What will be the Maximum Loss?

The loss is limited to the extent of premium paid. And when will this situation arise? when on expiry the Spot Price < Strike Price.

And what will be the Maximum Profit when buying a Call?

Theoretically we can say that the profit is Unlimited as the market rallies. Profit will only occur when Spot Price > Strike Price.

The payoff from a long position in a call option can be given by this equation.

= Max (S – E, 0) – C

Where,

E = Strike price

S = Price of the underlying security at maturity/ Spot price

C = Call option premium

Trading is ZERO SUM GAME. Profit for one person will be loss for other and vice versa. So, let us discuss a short call now.

A short call is simply the selling of a call option. It is a Bearish Strategy.

When to use it?

When you expect the spot price is less than the strike price, that means a bearish view on the market direction.

What will be the Maximum Loss?

Theoretically we can say Unlimited as the market rises.

And this loss will arise when: Spot Price > Strike Price

And Maximum Profit is Limited to the extent of premium received which will occur when

Spot Price < Strike Price

The payoff from a short position in a call option

= Min (E - S, 0) + C

Where,

E = Strike price

S = Price of the underlying security at maturity

C = Call option premium

Introduction to Put Options

An option that conveys the right to sell something is called a Put option. It gives the option to sell a stock at a predetermined price.

The put option buyer is betting on the fact that the stock price will go down and in order to profit from this view he enters into a Put Option agreement. In a put option agreement, the buyer of the put option can buy the right to sell a stock at a particular price irrespective of where the underlying/stock is trading at.

In markets, whatever the buyer of the option anticipates, the seller anticipates the exact opposite, and that’s how an efficient market exists.

So if the Put option buyer expects the market to go down by expiry, then the put option seller would expect the market to go up or stay flat.

A put option buyer buys the right to sell the underlying to the put option writer at a predetermined rate.

Example:

Assume Reliance Industries is trading at ₹1850/-

A put option buyer buys the right to sell Reliance to put option seller at ₹1850/- upon expiry. To obtain this right, put option buyer has to pay a premium to the put option seller. Against this premium put option seller will agree to buy Reliance, if the contract is exercised.

On expiry Reliance is at ₹1820/- then the option is exercised , so buyer of put option can demand the option seller to buy Reliance at ₹1850/- from him.

This means put option buyer can enjoy the benefit of selling Reliance at ₹1850/- when it is trading at a lower price in the open market (₹1820/-). Put option seller will be obligated to buy Reliance at ₹1850/-

If Reliance is trading at ₹1850/- or higher upon expiry (say ₹1870/-) it does not make sense for put option buyer to exercise his right and sell the shares at ₹1850/-. This is quite obvious since he can sell it at a higher rate in the open market.

An agreement where one obtains the right to sell the underlying asset at a pre-determined price on expiry is called a ‘Put option’

So three takeaway points from this example is:-

1. The buyer of the put option is bearish about the underlying asset, while the seller of the put option is neutral or bullish on the same underlying asset.

2. The buyer of the put option has the right to sell the underlying asset upon expiry at the strike price.

3. The seller of the put option is obligated (since he receives an upfront premium) to buy the underlying asset at the strike price from the put option buyer if the buyer wishes to exercise his right.

A long put, means buying a put option. It is a Bearish Strategy.

When to use: When we expect the spot price to be less than the strike price, and we are bearish on the market direction.

Maximum Loss: Limited to the extent of premium paid which will arise only when Spot Price > Strike Price.

Maximum Profit: It is theoretically Unlimited as the market falls and arises when Spot Price < Strike Price

The payoff from a long position in a put option can be given by the equation

= Max (E – S, 0) - P

Where,

E = Strike price

S = Price of the underlying security at maturity

P = Put option premium

The payoff from a short put position is exactly opposite of from long put. It is a bullish strategy and the payoff can be given by

= Min (E – S, 0) + P

We can Sum up Call and Put pay off by the following Table:

To clearly tabulate when a call and a put option is exercised or lapse, we have:

Need for Options

Previously we have learned so many different types of derivative instruments like Forwards, Futures, etc. So what is the need for Options? Well, there are a few reasons why options are required in trading? The reasons are discussed below:

Less capital required

In option trading, less capital is required compared to stock trading, because option price is only a small fraction of the underlying stock price. When a trader is confident that a stock price will move in a particular direction within a short term, he can invest in option rather than in stock itself to take advantage of the expected movement, because of the limited risk, high potential reward and the smaller amount of capital is required to control the same number of shares of stock.

Protection

Investor’s protection is an important part of trading. An investor who invests in stocks, put options can be used as a hedging tool to protect your stock from a price drop. When the stock price drops, the put option will increase in value, hence offsetting the loss in the stock. When the stock rises the put option would simply expire worthless when the expiration dates come and you will only lose the amount you paid to purchase the put option. So, as if you buy a put option as an insurance policy to protect your stock from a price fall.

Leverage

You can potentially have a greater percentage of return on investment from option trading than stock trading.

For example:

A stock price of company XX. Ltd (currently trading at ₹96) is expected to increase significantly over the next few weeks. The call option price for that stock with strike price of ₹95 and 30 days to expiration is ₹6.

If you buy 100 shares of that stock, you need to invest ₹9600 to purchase the stock. Assuming the stock price increases to ₹105 within 15 days you would gain ₹900 (10,500-9,600) or 9% (900/9,600).

But if you buy a call option contract for that stock instead, the cost will only be ₹600. When the stock prices rises to ₹105, the option price may increase to ₹11 and you can sell the option with a gain of ₹500 (1,100-600) or 83% (500/600).

As we can see, given the same number of shares, we get much higher % return using option than stock.

We must understand that Leverage is a two-sided sword. In case of losses, the losses are also amplified in options.

Difference Between Future and Option Contract

To better understand Option Contracts and how they differ from Futures contracts, here is a list of differences between the two:

Option Buying Vs Option Selling

Next, in this section, we will discuss the differences between Options Buying and Options Selling.

When you are trading options, you can either buy or sell option contracts. You may be wondering, which is better? Buying or selling options? Let us understand the nitty-gritties of selling and buying options.

When you buy an option there is someone selling it to you and vice-versa. Now suppose you are a seller of an option; you collect the option premium (at the time of executing the trade) from the option buyer. Your goal is to buy it back at a lower price, or the contract lapse so that the premium becomes zero. The buyer’s goal is to sell it at a higher premium than what was paid to enter the transaction.

There are several factors that affect the price of an option, but the primary three factors are time to expiration, price movement that is the direction of the underlying stock relative to the strike price, and volatility.

Now it has been seen that a seller of an option has 2/3rd chance of making profit where as a buyer of an option has only 1/3rd chance of making profit.

Why does selling options give you a higher probability of winning?

1st thing is - Time Decay is always in the favour of the Option Seller.

Options are a decaying asset. The premiums decay with the passage of time and they expire. So even if all the other factors that affect an option’s premium price, such as the price of the underlying stock, its volatility remain the same, that option will be worthless at expiration.

Time decay always works in favour of the option seller and against the option buyer.

2nd thing to note is that at any point of time the stock price can move in 3 directions: Up, down, or sideways. When you sell options, you can be in a profitable position when the price moves in the direction which you want it to move , or if it moves sideways, and even slightly in an undesirable direction.

Let’s take a look at an example by selling a call option. When you sell a call option, you normally sell a contract with a strike price that is higher than the current stock price. By entering in this trade, you collect the premium as being the option seller. Now once you have entered into this trade, the stock price can move in any direction, meaning the stock can either go down, it can remain unchanged, or it can go up by a little to be in a winning situation.

If you sold a ₹ 520 call option for underlying stock currently at ₹ 500 and took in ₹10 as option premium, the following could occur:

As it can be seen in the Table above, the option seller earns as long as the underlying price is below the strike price plus the premium received by him. The option buyer earns or is in profits only if the underlying price goes above the strike price, plus the premium paid.

When you are buying an option, there are two things which need to work in your favour. 1st is stock direction, and 2nd is volatility. If the volatility of the underlying doesn’t increase the premium value decreases, and option buyers face losses.

Moneyness of Options

After discussing the concept of Call options and Put options, in this unit we will discuss the ‘Moneyness of Options.'

Moneyness is a term which describes the relationship between the spot price of the underlying asset and the strike price which is the pre-determined price and the premium.

A clear understanding about Moneyness is required to choose the correct option in a given situation. It is one of the most frequently used option terminologies and all the option trading strategies stem from Moneyness. This concept will directly impact our decision-making process in options.

Example

Nifty Spot price is trading at ₹17200. And we are considering Nifty 17100 Call option. Now, suppose we assume that this option contract expires very next moment, so what is the minimum premium the seller is going to charge the buyer for this contract?

The seller of the contract is sure that this particular contract is going to get exercised, the buyer will exercise his contract as he will be able to buy NIFTY at 17100 where as currently its trading at 17200. So the loss which the seller will incur from the exercise of the option will be ₹100 (17200-17100).

This is the payoff from the call option. So, knowing that this contract expires next moment and it will be exercised, the minimum the seller should charge the buyer is ₹100 premium.

An option premium can be broken up into two – 'Intrinsic Value' of an Option premium and 'Time value' of an option premium.

Intrinsic Value of Options:

The intrinsic value of an option represents the current value of the option, how much worth it is. It’s the positive payoff for the Buyer. It represents what the buyer would receive if he decided to exercise the option right now. So, in accordance with our example it's ₹100.

The intrinsic value of an option is calculated differently depending on if it is a call option or a put option, but it always uses the strike price of the option and the price of the underlying asset.

For call options: Intrinsic Value = Max of (Price of Underlying Asset - Strike Price), 0

For put options: Intrinsic Value = Max of (Strike Price - Price of Underlying Asset), 0

Intrinsic value of options is never negative. It is either 0 or a positive number.

Time value of options:

The time value of an option is an additional extra amount a buyer is willing to pay over the current intrinsic value. Buyers of the options are willing to pay this because an option premium could increase in value before its expiration date. This means that if an option is months away from its expiration date, we can expect a higher time value on it because there is more opportunity for the option to increase or decrease in value over the next few months.

If an option is expiring today, we can expect its time value to be very little or nothing because there is little or no opportunity for the option to increase or decrease in value.

Time value is calculated by taking the difference between the option’s premium and the intrinsic value.

Time Value = Option Premium - Intrinsic Value.

We can conclude by saying that:

Option Premium = Intrinsic Value + Time Value

The moneyness of an option contract is simply a classification wherein each option (strike) gets classified as either – In the money (ITM), At the money (ATM), or Out of the money (OTM) option. This classification helps the trader to decide which strike to trade, given a particular circumstance in the market.

Understanding this option strike classification is very easy. All we need to do is figure out the intrinsic value.

If the intrinsic value is a positive, then the option strike is considered ‘In the money’. If the intrinsic value is zero the option strike is called ‘Out of the money’. The strike which is closest to the Spot price is called ‘At the money’.

The option chain helps you identify all the strikes that are available for a particular underlying and also classifies the strikes based on their moneyness. Besides, the option chain also provides information such as the premium price (LTP), bid –ask price, volumes, open interest etc. for each of the option strikes.

In The Money (ITM)

An in-the-money option has positive intrinsic value as well as time value.

A call option is in-the-money when the strike price is below the spot price.

A put option is in-the-money when the strike price is above the spot price

At The Money (ATM)

If the strike price is the same as the spot price, then it is called the “At-the-money” option.

An at-the-money option has no intrinsic value, it only has time value.

Out Of The Money (OTM)

An out-of-the-money option has no intrinsic value.

A call option is out-of-the-money when the strike price is above the spot price

A put option is out-of-the-money when the strike price is below the spot price

Factors affecting Option Premium

In our earlier units, there were several points where we discussed Option Premium. It is basically the current market price of an option contract. Here in this section, we will learn the factors that affect the options premium.

Let us understand these factors with the help of an analogy. Yesterday I was watching a Bollywood Thriller movie and I quite liked it. After the movie I was wondering what really made me like the movie. Was it the overall storyline, or brilliant acting by the cast or the nice direction by the director of the movie? Well, I suppose it was a mix of all the factors that made the movie enjoyable.

This also made me realize, there is a lot of similarity between a Bollywood movie and an options trade. Similar to a Bollywood movie, for an options trade to be successful in the market there are several forces which need to work in the option trader’s favor. These forces influence an option contract in real time, affecting the premium to either increase or decrease in real time.

There are six factors which affect the option premium. They are:

1. Underlying Security Price

Change in market price of an underlying security has a direct effect on Option Price. When the market price of underlying security increases, the Call Options Premiums increase while the Put Options Premiums decrease. On the other hand, when security price decreases, the Put Options Premiums increase while the Call Options Premiums decrease. Hence, we can say that the call option’s premium is directly related with underlying security price whereas put option’s premium is inversely related with underlying security price.

2. Option Strike Price

Different Strike Prices for an Option show different responses to change in market price of underlying security. Price change in Options prices is more sensitive for the Strikes which are near to the current price of the underlying security. The Strike Prices far away from the current price of the security see comparatively small change.

- As the strike price increases, the value of the call option decreases

- And as the strike price increases, the put option increases

Value of the call option is positively related with option strike price and value of put option is negatively related with option strike price.

3. Time to Expiration

Options have a limited life span thus their value is affected by the passing of time. As the time to expiration increases the value of the option increases. As the time to expiration gets closer the value of the option begins to decrease. Value of both put and call options are positively related with time to expiration.

The value begins to rapidly decrease within the last few days of an option's life. This is called as Time Decay. Some novice traders fail to recognise the importance of Time Decay, due to which they suffer losses unknowingly. Option Sellers use the Time Decay to their advantage.

4. Interest Rate

They don’t hold much significance for trading purposes. They indicate the interest rate incurred on the cost of carrying the entire trade value and the Dividend yield on it.

When interest rates rise a call option's value will also rise and a put option's value will fall.

To understand this concept, look at the decision-making process of trying to invest in IDFC ltd. while it is trading at ₹50. Say, we can buy 100 shares of the stock outright which would cost us ₹5,000.

Instead of buying the stock outright we can buy a (ATM) at the money call for ₹5.00. Our total cost here would be ₹500. Our initial outlay of cash would be smaller and this would leave us ₹4,500 left over.

We will also have the same reward potential for half the risk. Now we can take that leftover cash and invest it elsewhere such as Treasury Bills. This would generate a guaranteed return on top of our investment in IDFC. The higher the interest rate the more attractive the second option becomes.

Thus, when interest rates go up calls are a better investment so their price also increases.

On the other hand, if we look at buying a put versus a call, we can see a clear disadvantage.

The higher the interest rate the more attractive the call option becomes and when interest rates rise the value of put options drops.

5. Dividends

Options do not receive dividends so their value fluctuates when dividends are released. When a company declares dividends, they have an ex-dividend date. If you own the stock on that date you will be receiving the dividend. On this date the value of the stock will decrease by the amount of dividend.

As dividends increase a put option's value also increases and a calls' value decreases.

6. Volatility

Volatility is the degree to which price moves, whether it goes up or down. It is a measure of the speed and magnitude of the underlying's price changes. There are two types of volatility:

- Historical volatility

- Implied Volatility

Historical volatility refers to the actual price changes that have been observed over a specified time period. Options traders can evaluate this historical volatility to determine possible volatility in the future.

Implied volatility, on the other hand, is a forecast of future volatility and acts as an indicator of the current market sentiment. Implied volatility can be difficult to quantify, option premiums are generally higher if the underlying exhibits higher volatility because it may have higher expected price fluctuations.

The higher the volatility, the more people will think that the stock price will move in their preferred direction. Hence, options on highly volatile stocks are expensive.

Option Pricing

After we have learned the six factors that affect Option Premium, let us understand how options pricing is done.

How is pricing of Options done theoretically?

Option pricing theory uses different variables, which we discussed above (stock price, exercise price, volatility, interest rate, time to expiration), to theoretically derive the value of an option.

The primary goal of option pricing theory is to calculate the probability that an option will be exercised, or be in-the-money (ITM), at expiration. The most commonly used model to derive the fair value options is the Black-Scholes Model. The theory provides an estimation of an option's fair value which traders incorporate into their strategies to maximize profits.

In real life trading, options prices are determined in the open market and, the value can differ from the theoretical value. However, having the theoretical value allows traders to assess the likelihood of profiting from trading those options.

The Black Scholes model is perhaps the best-known options pricing method. So, let us discuss this particular model in the next unit.

Black Scholes Pricing Model

What is the Black Scholes Model?

The 'Black Scholes Model' is one of the most important concepts in modern finance both in terms of approach as well as applicability and is widely used by option market participants. Fischer Black and Myron Scholes together developed a formula to compute the prices of European calls and puts based on certain assumptions in order to eliminate the risk factor.

This is a straightforward model which explains that the asset price follows a geometric Brownian motion that looks like a smile or smirk with constant drift and volatility.

The Black-Scholes model states that by constantly adjusting the proportions of stocks and options in a portfolio, the riskless hedge portfolio can be created by investors where all market risks are eliminated.

What are the Inputs required in Black Scholes model?

The inputs in the Black Scholes model are affected by five basic factors. The inputs in this model are spot price, exercise price, time to expiration, stock volatility, and interest rate. Let's understand these inputs in a little more detail-

Spot Price: It is simply the market price of the underlying asset on valuation date. In case of illiquid assets, it may be a difficult input to find but under normal scenarios the closing market price can be used.

Strike Price: It is the price level at which the option holder has the right to buy or sell the underlying asset. This input will always be given in the option contract so you don’t need to worry about this.

Time to Maturity: It is the time period (in years) until which the contract expires.

Risk free Interest Rate: The yield on zero coupon government bond is usually taken as risk free interest rate.

Volatility: It is probably one of the most important input in option pricing model. You can calculate volatility in different ways.

Historical volatility can be calculated using historic price data for the movement of share price. Usually you should calculate data over a longer time frame say more than five years. However, there are many flaws in historical volatility as it assumes that the past will reflect the future which is not the case always.

Hence you should use forward looking measures like implied volatility to avoid this shortcoming and to make calculation more realistic.

Let’s understand the concept of implied volatility:

Implied Volatility is a volatility implied by the market price of trading options. Since the volatility is unknown (which is an input here) and the price is known, the pricing model is reversed to determine the volatility. You need to be aware of the volatility surface when using implied volatility. Volatility surface is three-dimensional representation of the relationship between volatility, option life and exercise price. So, in order to use implied volatility, the option from which the volatility is implied should have a relationship between volatility, option life and exercise price.

Assumptions of Black Scholes Model

Through this model, one can compute the value of stock options and can be used to compute the values of both call and put options. This model is based on a number of assumptions which are to be carefully studied in order to have a better grasp over the topic.

(i) Constant volatility: Volatility is a measure of how much a stock can move in the near term. It is assumed to be constant over time. This implies that the variance of the return is constant over the life of the option. However, in real life trading this condition doesn’t apply.

Volatility can never be constant in the longer term rather can be relatively constant in a very short-term horizon. This is the reason why some advanced option valuation model substitute with stochastic process generated estimates over Black-Scholes’ constant volatility.

(ii) No dividends: Next assumption is that the underlying stock does not pay any dividend during the life of the option which practically seems very unrealistic as most companies pay dividends to their shareholders.

A simple way of adjusting the Black Scholes models for dividends is to simply deduct the discounted value of a future dividend from the stock price.

(iii) Efficient markets: Another important assumption of Black Scholes model is that they assume markets to be fully efficient where all participants have equal access to available information and at the same time, the markets are assumed to be liquid. This assumption of an efficient market suggests that people cannot predict the price movement in a consistent manner. The Black-Scholes model assumes that stocks move in a manner referred to as a random walk. Random walk means that at any given moment in time, the price of the underlying stock can go up or down with the same probability. This is not the case in the real world as the market may remain inefficient for a prolonged period of time.

(iv) Log-normally distributed returns: Next assumption is that returns on the underlying stock are normally distributed. This assumption is very reasonable in the real world.

(v) Interest rates are constant and known: The Black Scholes model also assumes interest rate to be constant. Hence the model uses risk free rate to represent constant and known rate. So, the market participants can both borrow and lend at this rate but in the real world, risk free rate doesn’t exist.

(vi) No transaction costs and commissions: This assumption states that there are no barriers to trading i.e. there are no transaction costs or any commission associated with the buying or selling of assets.

(vii) European-style options: The Black-Scholes model assumes European-style options which can be exercised only at expiration date. It does not take in consideration American-style options that can be exercised at or before expiration of the contract, making it more valuable due to higher flexibility.

(viii) Liquidity: This model assumes that markets are perfectly liquid and you can purchase or sell any volume of stock or options at any point of time.

Black Scholes interpretation:

Keeping in mind the above assumptions, suppose there is a derivative security which is trading in the market. This security will have certain payoff at a future specified date, depending upon the stock price to that date. It is little surprising that the price of a derivative is determined at the current moment while the stock price follows a random walk which cannot be determined at the current time but in the future.

However, in case of European call or put option, Black Scholes stated that it is possible to create a hedged position where you will have a long position in the stock and simultaneously a short position in the option whose value will be independent of the stock price”. This dynamic hedging strategy resulted in a partial differential equation which guided the price of option which can be understood through the Black Scholes formula.

Black Scholes equation

The Black Scholes equation is a partial differential equation, which explains the price of an option over time. The equation is shown below-

The idea behind the equation is that you can easily hedge the option by buying and selling the underlying asset in just the right way and thus eliminating the risk factor. As per this hedge, there is only the right price for the option which is explained by the Black Scholes formula.

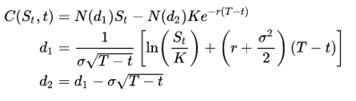

Black Scholes formula

The price of a European call and put option can be computed using the Black Scholes formula. This price is consistent with the above discussed Black Scholes equation as the formula can be obtained by solving the equation for the corresponding terminal and boundary conditions.

In terms of the Black–Scholes parameters, the value of a call option for a non-dividend-paying stock is:

Based on put–call parity, the price of corresponding put option is-

Where,

- T-t is the time to maturity (in years)

- N is the cumulative distribution function of the standard normal distribution

- St is the spot price of the underlying asset

- r is the annual risk free rate (expressed in terms of continuous compounding)

- σ- is the volatility of returns of the underlying asset

- K is the strike price

Black Scholes Option Pricing model played a very important role at articulating pricing of options and corporate bonds on the assumption that a risk-free interest rate existed. Even today it is used for estimating the worth of options but it is applied mostly in academics and in portfolio management departments of big institutions.

There are a number of reasons for wide use of this model in spite of several loopholes. The most important one is that it provides a framework for options pricing and gives a good approximation to the pricing of options. Another important reason for studying the Black-Scholes theory is that it is used as a standard in the financial world. In many cases, traders quote the Black Scholes volatility to each other than actual prices of the option.

Option Greeks

As we have learned earlier, Option premiums change with changes in the factors that determine option pricing, i.e., factors such as strike price, volatility, term to maturity, etc. The sensitivity of option premium to each of these factors is known as 'Option Greeks.'

For a successful options trade in the market there are several forces which need to work in the option trader’s favour. These forces are together called ‘The Option Greeks’. These forces influence an option contract in real time, affecting the premium to either increase or decrease. These forces not only influence the premiums directly but also influence each other.

The five Option Greeks are:

- Delta

- Gamma

- Theta

- Vega

- Rho

We will discuss all of the above in our subsequent units.

Delta

Firstly, let us understand ‘Delta.’

The Delta measures how an options value changes with respect to the change in the underlying. Means, the Delta of an option helps us answer that –

By how many points will the option premium change for every 1-point change in the underlying?

Delta captures the effect of the directional movement of the market or underlying on the Option’s premium.

Delta value ranges from 0 to 1 in case of call options

Delta value ranges from 0 to -1 in case of Put options

Why is delta negative for a put option and positive for a call option?

We have discussed this earlier, that with one unit increase in spot price, call premiums increase and put premium decrease. If the call premium increases with spot price increase, the delta of call options has to be positive and vice versa.

Example:

Consider Nifty is at 17288

Option Strike = 17250 Call Option

Premium at which it trades is = 133

And Delta of the option = + 0.55

Now say Nifty is expected to reach 17310

What will be the option premium value then? We know the Delta of the option is 0.55. We are expecting the underlying to change by 22 points (17310 – 17288), hence the premium is supposed to increase by

= 22*0.55

= 12.1

Therefore, the new option premium is expected to trade around 145.1 (133+12.1)

A delta of 0.55 indicates that for every 1-point change in the underlying, the premium is likely to change by 0.55 units.

The delta helps us evaluate the premium value based on the directional move in the underlying. And this is extremely useful information to have while trading options.

- Call Options have Positive Delta

- Put Options have Negative Delta

- OTM options have a delta value between 0 and 0.5, ATM option has a delta of 0.5, and ITM option has a delta between 0.5 and 1.

We can tabulate this to give us a better understanding:

Gamma

Secondly, we are going to discuss ‘Gamma’.

Gamma is the rate of change in an option's delta per 1-point move in the underlying asset's price. Gamma is an important measure of the convexity of a derivative's value, in relation to the underlying.

Example.

Nifty Spot is at 17312, strike under consideration is 17400, and option type is Call Option (CE).

What is the approximate Delta value for the 17400 CE when the spot is 17312?

Delta should be between 0 and 0.5 as 17400 CE is OTM.

Let us assume Delta is 0.4

Now if the NIFTY spot moves from 17312 to 17400, what do you think is the Delta value?

Delta should be around 0.5 as the 17400 CE is now an ATM option and if Nifty spot moves from 17400 to 17500, what do you think is the Delta value? Closer to 1 as the 17400 CE is now an ITM option. Assume 0.8.

If the Nifty Spot cracks heavily and drops back to 17300 from 17500, what happens to delta? With the fall in spot, the option has again become an OTM from ITM, hence the value of delta also falls from 0.8 to let us say 0.3. What can we understand from this example?

When the spot value changes, the moneyness of an option changes, and therefore the delta also changes.

The Gamma of an option measures this change in delta for the given change in the underlying. In other words, Gamma of an option helps us answer this question – “For a given change in the underlying, what will be the corresponding change in the delta of the option?”

Theta

Thirdly, we will discuss ‘Theta’.

What is theta?

Theta is a measure of the rate of decline in the value of an option due to the passage of time. Theta is generally expressed as a negative number and can be thought of as the amount by which an option's value will decline every day.

We know, Premium = Intrinsic Value + Time Value

Intrinsic value is always a positive value or zero and can never be below zero. It’s a relationship between spot price and strike price.

Time value is what is being charged on account of passage of time and volatility. Time as we know moves in one direction.

Keeping the expiry date as the target time, as time progresses, the number of days for expiry gets lesser and lesser. Given this let me ask you this question – With roughly 18 trading days to expiry, traders are willing to pay as much as ₹100/- towards time value, will they do the same if time to expiry was just 5 days? Obviously, they would not right? With lesser time to expiry, traders will pay a much lesser value towards time.

“All other things being equal, an option is a depreciating asset. The option’s premium erodes daily and this is attributable to the passage of time”.

All options – both Calls and Puts lose value as the expiration approaches. The Theta or time decay factor is the rate at which an option loses value as time passes.

Theta is expressed in points lost per day when all other conditions remain the same.

Theta is a friendly Greek to the option seller. Remember the objective of the option seller is to retain the premium. Given that options lose value on a daily basis, the option seller can benefit by retaining the premium to the extent it loses value owing to time.

Vega and Rho

Having understood Delta, Gamma, and Theta we are now all set to explore the last two Option Greeks: Vega and Rho.

What is Vega?

Vega, is the rate of change of option premium with respect to change in volatility.

What is volatility?

Volatility is not just the up and down movement of markets. Volatility is a measure of risk and is estimated by standard deviation. We can estimate the range of the stock price given its volatility. Larger the range of a stock, higher is its volatility or risk. It’s the degree of uncertainty attached to a stock price.

Imagine a stock is trading at ₹100, with increase in volatility, the stock can start moving anywhere between 90 and 110. So, when the stock hits 90, all PUT option writers start sweating as the Put options now stand a good chance of expiring in the money. Similarly, when the stock hits 110, all CALL option writers would start panicking as all the Call options now stand a good chance of expiring in the money. Therefore, irrespective of Calls or Puts when volatility increases, the option premiums have a higher chance to expire in the money.

Example:

You want to Sell 500 CE options when the spot is trading at 475 and 10 days to expire.

Clearly there is no intrinsic value but there is some time value. Hence assume the option is trading at ₹20. You may write the options and pocket the premium of ₹20/-

However, what if the volatility over the 10-day period is likely to increase – maybe election results or corporate results are scheduled at the same time. Will you still go ahead and write the option for ₹20? Maybe not, as you know with the increase in volatility, the option can easily expire ‘ITM’ hence you may lose all the premium money you have collected.

The option's Vega is a measure of the impact of changes in the underlying volatility on the option price. Specifically, the Vega of an option expresses the change in the price of the option for every 1% change in underlying volatility.

Options tend to be more expensive when volatility is higher.

Thus, whenever volatility goes up, the price of the option goes up and when volatility drops, the price of the option will also fall. Therefore, when calculating the new option price due to volatility changes, we add the Vega when volatility goes up but subtract it when the volatility falls.

What is Rho?

Rho is the rate at which the price of a derivative changes relative to a change in the risk-free rate of interest. Rho measures the sensitivity of an option or options portfolio to a change in interest rate.

For example, if an option or options portfolio has a rho of 1, then for every percentage-point increase in interest rates, the value of the option increases 1%.

Margins for Options Trading and Settlement

Finally, in this last section, we will learn the different types of margins in options trading and how options contracts are settled.

The investors who buy option contracts are required to maintain the margin requirements on the position. Based on the position taken by the investor, the margin requirement varies. Traditionally investors need to deposit 100% of the options premium in 2 business days after settlement but it has evolved gradually over the period.

Let’s understand margins involved in buying and selling of options:

We know that option buyers can have a limited loss or unlimited profit. On the other hand, option sellers face a situation of limited profit or unlimited losses.

Thus, option buyers in order to enjoy the upside or the downside as the case may be, and hence have to pay a certain premium to the option seller. While option sellers are required to pay margin money in order to create this position.

Margin money is often measured as a % of the total value of the open position. Option buyers can have a limited loss or unlimited profit thus required to pay the premium to enjoy the upside or the downside. On the other hand, option sellers may have a situation of limited profit or unlimited losses and hence they need to deposit margin.

Margin for options buyer

For the buyer, they need to pay only the premium and not the full price of the contract. The exchange transfers this premium to the broker of the option seller who in turn transfers it to the client.

So, the minimum loss to the option buyer is restricted to the premium amount.

Margin for options seller

The option seller, on the other hand, has a potential for unlimited loss.

Thus, the seller has to deposit margin with the exchange as a security in case of huge loss due to adverse price movement in the option price. This amount is levied on the contract value and the amount is denoted in % term as dictated by the exchange.

Usually, this % value is created based on the volatility of the price of the underlying asset and the option. Higher the volatility, higher is the premium.

Margin for options example

Mr. A sells 1 lot (lot size is 600 shares) of call option of Infosys. The premium received is Rs 10 for the strike price of 970 and we assume a margin of 20%.

The option position stands at 582000 (600 x 970). Thus, the margin amount is Rs 116400 (582000 x 20%).

Types of Margin

- Initial margin– It requires the minimum amount of capital or equity that an investor must provide during purchase. It is done to prevent over speculation and excessive trading. It is that margin requirement which investors talk about when dealing with margin trading.

Until there is enough margin in the account i.e. greater than or equal to the initial requirement, the investor can freely use his account. However, if the margin goes below the initial margin requirement, it will lead to a situation of restricted account which requires investors to bring back to the initial level. - Maintenance margin– It is the minimum margin amount which an investor must maintain at all time in the margin account.

Say if the margin goes back below the maintenance margin level, the investor will get a call initially to remedy the position or else the broker has an authority to sell the required equity to bring back to the initial level.

It protects both investors and the brokerage house. The broker does not have to absorb excessive investor losses while the investor is in a situation to avoid being totally wiped out.

Options Margin calculator

Click here to compute the margin from the Options Margin Calculator

Options Settlement

An option can be settled either through physical settlement or through cash. In case of physical delivery, options require actual delivery of the underlying asset.

Whenever we sell or purchase any option, we can exit before the expiry date by taking an offsetting position in the market or we can hold the position till the maturity date where the clearinghouse settles the trade.

Conclusion

Now that we are at the end of this module, let's do a quick recap of what we have covered:

- Concept of Option Contract

- Common Option Terminologies

- Call Options & Put Options

- Factors affecting option premium

- Black Scholes Pricing model

- Option Greeks

- Option Trading Margins

Though we have covered a lot more in this module, the above topics are extremely important before diving into options trading. This module has surely removed all the complexities that you had related to options trading. But wait, there is more to learn. We have designed many such modules at ELM School that will provide you with enormous knowledge about not just options or derivatives but overall financial markets. So, be sure to check out all the modules that we have curated for you.