Role of RBI

Introduction to Role of RBI

The 'Reserve Bank of India' (RBI) is the central bank of our country. A central bank controls all banks, financial institutions and financial firms in India. So, to explain the role of the RBI, we have a story to share that will give more clarity to your understanding of this module.

Ram had been a curious child since he was a little boy. As he was growing up, he was fascinated by the mechanisms that contributed to the working of a country. He always wondered how the government had so much money to spend for the welfare of the people. He went to the bank with his father regularly. He used to get puzzled by the amount of money there and pondered on how the transactions were taking place. Over time his questions tripled in number and the need for answers grew simultaneously. He sat down with his father one day and was bombarded with multiple questions. His father laughed and said that the first step to understand the financial workings of a country is to know about the Central Bank and its functions. Here’s what he had to say:

Overview of Reserve Bank of India

The Reserve Bank of India was established on April 1, 1935. It was originally a private entity, but its reins were handed over to the Government of India after the nationalization program. The RBI is regarded as India’s central bank and regulatory body under the jurisdiction of the Ministry of Finance.

Every single task that an individual working in the RBI undertakes has an impact on the entire country; the poor as well as the rich get affected by its policies and working. The RBI is a statutory body that performs a number of onerous functions.

Role of RBI: Functions & Objectives

What is the role of RBI?

The RBI is the central bank of India. It was established in 1935 under a special act of the parliament. It is responsible for determining the country's monetary policy. The main role of the RBI is to maintain financial stability and to ensure adequate liquidity in the economy. The following are the main functions that the RBI performs dutifully:-

Enhance your knowledge on trading strategies. with our online share market courses. Enroll now for a deeper understanding of financial market in India.

1) Monetary management:- One of the major functions of the RBI is the formulation and smooth execution of the monetary policy. Monetary policy makes use of various policy instruments that influence the cost and availability of money in the economy. The objective remains to promote economic growth and ensure stability of prices. It ensures a smooth flow of credit to the productive sectors of the economy.

2) Issuer of Currency:- The management and issuance of currency is a vital central banking function. The RBI is responsible for the design, production, distribution and the overall management of the nation’s currency. It works to ensure a sufficient supply of clean and genuine notes across the state. It works to reduce the risks of counterfeit. Counterfeited notes are often used for terrorist financing which have various ill-effects.

3) Banker and debt manager of the government:- The RBI manages the government’s banking transactions. The Government of India also deposits its cash balances with the Reserve Bank. It can also act as a banker to any state government. It appoints other banks to act as its agents for carrying out the transactions on behalf of the government. It also manages public debt and issues new loans on behalf of the Central and state governments.

4) Banker to banks:- The settlement of inter-bank transactions is also the function of the RBI. This is usually done through the mechanism of a “clearing house” where banks present cheques and other such tools for clearing. The Central bank acts as the common banker among all the various banks.

5) Lender of the last resort:- When a commercial bank fails to obtain funds from the available sources then the Central Bank issues loans to it as a “lender of the last resort”. It can come to the rescue of any bank by supplying it with the needed liquidity when no other institution is willing to extend credit to it.

6) Financial regulation and supervision:- The RBI’s regulatory and supervisory functions are quite broad. It strives to maintain overall financial stability through various policy measures. It aims to achieve orderly development and conduct of banking operations, liquidity and solvency of banks.

7) Keeps a check on the growth of inflation:- The RBI maintains an inflation target of 4% with a +/- 2% tolerance band and deems it to be appropriate for the next five years. Whenever the RBI lowers the interest rates, people get to borrow loans from the commercial banks at a reduced rate. This in turn places more money in the hands of the general public, which boosts their purchasing power and demand for stocks. This heightened demand raises the prices of goods and in turn causes inflation. Similarly, when the banks increase the interest rates, the amount of borrowing from the banks decreases. People have less purchasing power and the demand for stocks decreases. The RBI controls inflation in this manner.

8) Acts as the custodian of foreign exchange reserves:- The Central Bank also functions as the custodian of the nation’s foreign exchange reserves. It focuses on the maintenance of market’s confidence in monetary and exchange rate policies. It helps to reduce the costs at which the foreign exchange resources are available to market participants.

9) Foreign exchange management:- The RBI oversees the foreign exchange market. It has also permitted foreign investment in almost all sectors.

10) Over-sees market operations:- The Central Bank operationalises its monetary policy through its operations in government securities, foreign exchange and money markets. It also carries out regulation and development of money market instruments such as, term money market, repo market, etc.

11) Developmental role:- The RBI takes an active role in supporting and enhancing developmental activities in the country. It ensures that the productive sectors of the economy get enough credit and creates institutions to build financial infrastructure. It also works to guarantee banking services to all.

It is understood that RBI has a significant role in the country’s economy. But there are some defined objectives of the RBI. They are:

Each of the above objectives are explained in the upcoming units.

How RBI controls Inflation?

The primary objective of the Central Bank is to control inflation.

Inflation refers to a sustained rise in the prices of goods & services. It results in a decline in the purchasing power of the people over a period of time.

The Consumer Price Index (CPI) and The Wholesale Price Index (WPI) are the accepted instruments in India for tracking inflation. It measures the average price change in a number of commodities and services. For instance, a sudden decrease in the amount of oil supply, leading to increased oil prices, can cause cost-push inflation. Inflation can occur when-

1) The cost of goods increases because of an increase in the cost of raw materials needed to manufacture such commodities.

2) There is an increased demand in the market for some goods and services. Consumers then become willing to pay even more for these products.

Inflation can be viewed in both positive and negative light. It is viewed as positive when it helps to boost consumer demand and consumption. This influences economic growth by encouraging producers to produce more to meet the increased demand. On the other hand, extremely high inflation can signal an overheated economy. It lowers the purchasing power of people drastically. It increases the cost of borrowing and reduces employment. Inflation also encourages spending. The urge to spend and invest more at the time of inflation tends to boost it even further, which creates a potentially disastrous feedback loop. It discourages saving and reduces economic growth by increasing the cost of living. This means that even as we save and invest, our accumulated wealth buys less and less with the mere passage of time.

Thus, inflation reduces the purchasing power and eats away the real returns on savings and investments.

Central banks use inflation targeting in order to keep economic growth steady and prices stable. The Reserve Bank of India has set a target inflation band of 4% +/- a band of 2%. By raising interest rates or restricting the flow of money supply in the country the RBI aims to keep the inflation in check. A lower interest rate tends to result in more inflation. When the interest rates are low, individuals and businesses tend to borrow more money from the commercial banks. This leads to a smooth flow of money in the economy. The purchasing power of people increases and thus their demand for various goods and services increases. This leads to heightened demand for goods and, in turn, causes inflation. Conversely, an increased interest rate makes people borrow less. Their purchasing power reduces, and so does the demand for commodities. This helps to keep inflation in check.

How does RBI impacts the Growth Rate?

The next objective of the Central Bank is to ensure that the economy grows at a smooth pace.

One of the ways to measure economic growth is to measure GDP growth.

GDP stands for Gross Domestic Product and is the total monetary value of all final goods & services produced in an economy at a given time period.

A rise in GDP signifies a rise in total output. It is presumed that this output is sold in the market and exchanged for money. Hence, with a rise in total output, the corresponding income of households is likely to increase.

A more accurate measure to use is the Per Capita GDP i.e. (Total Market value of Goods & Services) / (Total population)

The Reserve Bank of India aims to influence economic activity by using its monetary policy tools discussed previously. It ensures the flow of credit to the most productive sectors of the economy and therefore keeping the engine well oiled.

How does RBI maintain Financial Stability?

The objective of the RBI is also to maintain financial stability in the country. Financial stability can be defined in terms of a nation’s ability to facilitate and enhance economic progress by managing risks and absorbing shocks. The financial markets and the various financial institutions are resistant to economic shocks. This stability is important because it represents a sound financial system.

Rapid liberalisation of the financial sector, an inadequate economic policy, inefficient methods for resource allocation and poor market discipline can be factors for financial instability. A stable financial system is competent enough to efficiently allocate resources, assess and manage financial risks, and maintain the levels of employment. A stable economic system absorbs the shock beforehand with the help of self-corrective mechanisms. It refers to a condition in which the financial institutions are adept to carry out their financial transactions without requiring any external assistance, such as that of the government.

Stability of financial markets enables economic agents to raise and operate funds freely. Stability of financial infrastructure is used to define a condition where the financial system works to ensure that both the financial safety net and the payment and settlement system are running effectively. It is an essential condition as it ensures a healthy development of the entire economy.

A credit-rating company called ICRA Limited (formerly known as Investment Information and Credit Rating Agency of India Limited) was established in 1991 to provide independent, well-researched and expert credit risk opinions to borrowers in relation to their borrowing activities. It is essentially the second largest credit rating agency in India after CRISIL (formerly Credit Rating Information Services of India Limited). It provides ratings, research, risk and policy advisory services. A credit rating agency does researche and analyze the financial strength of several companies and government entities. They help investors in identifying the company’s ability to pay debts and to assess the level of risk involved.

RBI Monetary Policy

Monetary policy refers to the macroeconomic policy as defined by the central bank of a state. It consists of management of money supply and of interest rates. With its help, the Central bank increases or decreases the amount of money/currency in circulation around the state at any given time. Similarly, The RBI uses monetary policy to secure economic objectives such as inflation, consumption, growth and liquidity. For example, buying or selling of government securities through open market operations. The principal objective of monetary policy is to reach and maintain a low and stable inflation rate, and to secure a long-term GDP growth trend. It also aims to generate more employment. There are two types of monetary policies-

1) Contractionary monetary policy

It is used to decrease the amount of money flowing through the economy. It can be achieved by selling government bonds or by raising the interest rates.

2) Expansionary monetary policy

It is used to increase the amount of money supply in the economy. It can be achieved by such actions as decreasing interest rates or by the purchase of government securities by the central banks.

Monetary policy is implemented by the usage of monetary policy tools of the RBI. The three main policy tools are:

a) Repo rate (policy rate) - In India, the commercial banks can borrow funds from The RBI if they have a temporary deficit in their reserves. The rate at which the banks borrow reserves from the central banks is referred to as the discount rate. For the Reserve Bank of India, it is called the repo rate. The central bank purchases securities from the other banks that in turn, agree to repurchase these securities at a higher price later. The difference between the repurchase price and the purchase price is the rate at which the central banks lend to the other banks. A lower repo rate encourages lending and decreases the interest rates. A higher repo rate has the opposite effect, it decreases lending and increases the interest rate.

b) Reserve requirements – It refers to the percentage of deposits that the banks are required to maintain as reserves with the central bank. By increasing this percentage, the central bank constructively decreases the funds that are available for lending and the flow of money supply, which would increase the interest rates. A decrease in the reserve requirement will increase the funds that are available for lending and money supply, which will lower the interest rates.

c) Open market operations – The process of buying and selling of securities by the central bank is referred to as open market operations. Buying of securities by the central banks makes more funds available for lending. The money supply increases and the interest rates tend to decrease. The sale of securities by the central banks has the opposite effect. It reduces the amount of funds available for lending and the money supply which increases the interest rates.

Changes in the monetary policy can also affect economic growth, inflation, interest rates and the foreign exchange rates. The effects of a shift toward an expansionary monetary policy include:-

- The buying of securities by the central bank increases the cash reserves.

- Banks become more willing to lend reserves to one another which leads to a decrease in the rate of interbank lending.

- Long-term interest rates tend to decrease.

- The decrease in long-term interest rates leads to increased levels of business investment in plants and equipment.

- The decrease in long-term interest rates also causes the currency to depreciate in the foreign exchange market.

- Lower interest rates increase the purchasing power of people significantly.

- Depreciation of currency results in an increased foreign demand for domestic goods.

- Increases in consumption, investment, and exports increase aggregate demand.

- An increase in aggregate demand increases inflation, employment and the GDP rate.

Government's Fiscal Policies

Father continues, “As we can understand the importance of RBI and its monetary policy, we should also know the importance of Government’s role in the economy, how even the policies taken by the government i.e. the Fiscal Policies also affect everyone in the society, from the poorest to the richest!”

Ram to his astonishment said “Oh really? So like RBI controls the economy with Monetary policy, our government’s weapon is the Fiscal policy!” “Yes!” said father, and all the steps that would be taken or has taken by the government is stated in the government’s budget! The term budget is derived from the French word "Budgette" which means a leather bag or a wallet. Budget is most important financial information document of the government. It is a statement of the financial plan of the government. It shows the income and expenditure of the government during a financial year, which in India runs from 1st April to 31st March.

Whether to raise or cut taxes, whether to reduce taxes across the board or reduce them for low and middle-income families; how much to spend on education, defence, infrastructure, social development, etc these and many related issues involve the fiscal policy.

Union Budget Categories

The Union budget of any particular nation consists of an estimation of revenue expenses and income over a specified future period of time. It is also called the “annual financial statement" as it is a statement of the estimated income and expenditure of the government for the upcoming annual year. It keeps a record of the government’s finances for the fiscal year that extends from 1st April to 31st March. The budget is presented before the people by the Union Finance Minister every year. It is usually formulated and re-evaluated over varying intervals of time. The Union budget is classified into two categories:

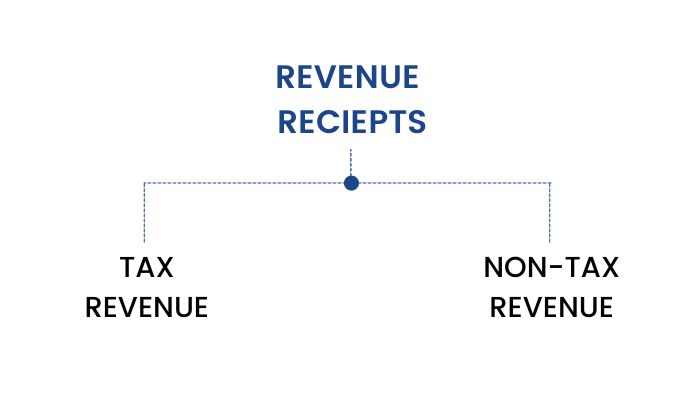

1)Revenue budget

It includes the government’s revenue receipts and expenditure. It is again of two types, tax and non-tax revenue. It refers to the expenditure incurred by the day-to-day functioning of the government and by the various services that are provided to the citizens. If the revenue receipts are lesser than the revenue expenditure, then a revenue deficit occurs.

2)Capital budget

It consists of capital receipts and payments of the government. Capital expenditure involves the money spent on the development of machinery, equipment, infrastructure, education facilities, health facilities and the like. Loans taken from the foreign governments, general public and the RBI all form a part of the government’s capital receipts. When the government’s expenditure is more than its total revenue, a fiscal deficit occurs.

Depending on the estimates of revenue and expenditure, budgets are classified into three broad categories:-

a)Balanced budget – In a balanced budget, the estimated government expenditure shall be equal to the estimated revenue in a given financial year. This type of a budget thwarts wasteful expenditure by the government. A balanced budget does not indicate financial stability in times of deflation due to the absence of any scope for extra expenditure. A balanced budget is not considered suitable for developing nations because it restricts the scope of government expenditure on schemes devised for the welfare of the public.

b) Surplus budget – In a surplus budget, the estimated government expenditure is less than the estimated revenue in a given financial year. This means that the government’s earnings generated from taxes is greater than the expenditure incurred on public welfare. This extra money can be used to pay dues which reduces the payable interest and helps economic growth in the long-run. Such a budget can be used in times of inflation. It is not an option during times of deflation, recessionary periods and during economic slowdowns.

c) Deficit budget – In a deficit budget, the estimated government expenditure exceeds the estimated revenue of the government in a given financial year. This type of a budget comes in handy at times of economic recessions and also helps in increasing the employment rate. It bolsters economic growth. The government usually covers the deficit amount by borrowing from the public or through government bonds. This type of a budget can cause excessive expenditure on the part of the government and also result in debt accumulation.

Since our independence in 1947, there have been a total of 73 annual budgets, 14 interim budgets and four special budgets, or mini-budgets.

Government's Revenue Receipts

Revenue receipts can be defined as the proceeds of taxes, interest and dividend on investments done by the government, taxes and other receipts for services provided by the government. They can be defined as income receipts of the government from various sources. Government revenue is quite literally the medium for government expenditure. Taxation is the most important source of income for all governments. Taxes can be defined as an involuntary fee levied on individuals, corporations, and institutions to finance government activities. Tax revenue forms a major part of the Union Budget. Taxes are collected both from direct sources and indirect sources.

1)Direct Tax

Direct tax is the tax that is paid directly by individuals and companies to the government, without the involvement of any intermediaries. For instance, income tax, wealth tax, corporation tax, property tax are all direct taxes. The higher the capability of paying is, the higher the taxes are. It promotes equality among the citizens as each person is charged according to their own incomes. The burden of paying direct taxes cannot be shifted to another person. The collection of direct taxes is however, a long and slow process.

2)Indirect Tax

Indirect taxes are those taxes that are collected by intermediaries from individuals and corporations. For instance, Goods and Services Tax (GST), Sales tax and Excise tax are all indirect taxes. These taxes can be passed on to another entity. We pay indirect taxes on every item that we purchase as a consumer. This is because taxes are imposed on all sorts of goods and services. People do not feel like they’re being taxed because indirect taxes are included in extremely small amounts. Their collection is relatively much easier.

Revenue receipts of the government are divided into two broad categories:-

a)Tax revenue receipts – Tax revenue includes proceeds of taxes and other duties that the government imposes on the public and the various corporations. The sum of all these receipts from taxes are called tax revenue receipts. They can be from direct or indirect taxes.

b)Non- tax revenue receipts – It is the recurring income of the government that is generated by sources other than taxation. Some of the major sources of non-tax revenue are interests that are received by the government on various loans, power supply fees, license fee, fines and penalties, grants from various organizations, forfeitures etc.

Fines and penalties are imposed by the government for the non-payment of taxes.

Many enterprises are owned and managed by the government. The profits received from them is an important source of non-tax revenue. For example, in India, the Indian Railways, Oil and Natural Gas Corporation (ONGC), Steel Authority of India (SAIL), Dredging Corporation, amongst other companies are owned by the Government of India. The profit generated by them is a source of revenue to the government.

Gifts and grants are received by the government when there are natural calamities like earthquakes, floods, famines, etc. Citizens of the country, foreign governments and international organizations like UNICEF, UNESCO, etc. donate during times of natural calamities.

Special assessment duty is a type of levy imposed by the government on the people for getting some special benefit. For example, in a particular locality, if roads are improved, property prices tend to rise in the future. The property owners in that locality will benefit due to the appreciation in the value of property. Therefore, the government imposes a levy on them which is known as special assessment duties.

What are Capital Receipts?

Capital Receipts are receipts which create a liability or result in a reduction in assets.They are obtained by the government by raising funds through borrowings, recovery of loans and disposing of assets.

The main items of Capital receipts are loans raised by the government from the public through the sale of bonds and securities, borrowings by government from RBI and other financial institutions through the sale of Treasury bills are also included in the capital receipts, loans and aids received from foreign countries and other international organizations like International Monetary Fund (IMF), World Bank, etc, receipts from small saving schemes like the National saving scheme, Provident fund, etc, recoveries of loans granted to state and union territory governments and other parties. So these are the capital income sources of the government.

Government's Revenue Expenditure

Now, let us see the expenditure side of the government. Broadly there are two branches of expenditure like income, the Revenue Expenditure and the Capital Expenditure.

Revenue expenditure is the expenditure incurred for the routine, usual and normal day to day running of government departments and provision of various services to citizens. It includes both development and non-development expenditure of the Central government. Usually expenditures that do not result in the creation of assets are considered revenue expenditure.

In general revenue expenditure includes expenditure by the government on consumption of goods and services, expenditure on agricultural and industrial development, expenditure on Scientific research, education, health and social services, expenditure on defense and civil administration, expenditure on exports and external affairs, grants given to State governments, payment of interest on loans taken in the previous year and expenditure on subsidies.

Capital Expenditure

Capital expenditure is the expenditure of the government that results in the creation of physical assets or a depletion in the financial abilities of the government. This includes expenditure incurred on buildings, land, equipment, machinery and loans and advances made by the central governments to the state governments. Capital expenditure forms a part of the government spending that is used in the creation of assets like schools, colleges, hospitals, roads, bridges etc. It also includes the acquisition of equipment and machinery by the government for defence purposes. It could also consist of investments that would yield profits or dividends in the future.

A high amount of capital expenditure would lead to rapid economic growth as the government invests more towards the creation of assets and the development of infrastructure. It reduces liabilities as well.

Capital expenditure which results in the creation of assets are as follows:-

a) Expenditure incurred on purchase of property, buildings, machinery, equipment and the like.

b) Investments made in shares. Loans given by the central banks to state governments, foreign governments.

c) Expenditure incurred for the acquisition of valuables.

This type of expenditure adds to the capital stock of the economy and increases the nation’s capacity to produce more in the future. Repayment of loans also forms a part of capital expenditure as it reduces the government’s liability.

Conclusion

So, you see, the role of RBI is not limited to its monetary policy. It has a much bigger role to play in our economy. Yes, of course, being the central bank of our country, its main objective is to control the money supply in the economy and keep inflation at a healthy range so that the economy can grow to its full potential. RBI is the banker to the Government of India. It manages the revenue and expenditure of the government so that it can focus on the social welfare and economic prosperity of the country. We hope you have enjoyed learning with us. There are more such interesting modules on ELM School. Do check them out as well!