100 FAQ's on Basic Finance

100 Most Asked Finance Questions

This module will help you understand the numerous financial jargons that are used daily by several working professionals in the finance industry. We have tried to answer the 100 most asked questions related to finance. Yes, 100 questions seem lengthy, but once you go through all the answers, you will indeed become more knowledgeable in the field of finance.

So let us get started!

When and why should you start saving?

Savings is the part of income that is kept after meeting our necessary expenditures (utility bills, domestic expenses, etc). When we come across situations like setting up a new business, investing in some expensive items or any financial emergency (medical cost, unexpected job loss) – one can easily deal with such situations provided he has enough savings.

Suppose you start saving at age 25 and your friend starts at age 35 with Rs 5000 @12%, till the age of 60 years, so let’s u see how much each one of you would save.

Saving early will help to enjoy the power of compounding, which means an increase in the value of investment because of reinvestment of the interest earned to grow the principal amount.

Have you ever thought about how much you should save every month?

The exact amount of savings and spending depends from person to person and should be decided depending on your financial goals, your income level, and your monthly expenditure.

To get you started, thumb rules could be of great help.

“Pay yourself first” is the first rule in personal finance. It means that you should first save money from your monthly income before spending it. Firstly, identify your goals, calculate the inflation (increase in the price level) adjusted requirement, and then make sure that your income gets transferred from your salary account to your savings account every month.

Another rule that could help you segregate your income into savings and expenditures is the very popular 50-30-20 rule.

As per this rule, one should assign 50% of their disposable income towards essential expenditures, 30% of it towards non-essential expenses, like going out to eat. The remaining 20% should be assigned toward your savings and investments.

How is investment different from Savings?

Investment means allocating income with the expectation of some future benefit or profit. When an asset or an item is acquired with the purpose of letting it grow so that you can earn profit out of it, it is an investment.

Generally, investments are made in two things in mind:

a. Capital appreciation

b. Income generating plans

So, when you purchase stocks, mutual funds, real estate, fixed deposits, etc. you are putting your money to work for you as these instruments will either appreciate in future or will keep on giving regular returns till the time you are holding them.

So, how is savings different from an investment?

- Savings are made for short-term goals, whereas investments are for achieving long-term goals.

- Savings funds are easily accessible like we can withdraw from our savings bank account anytime we want. But, invested funds are difficult to access, such as corporate bonds, which have a fixed maturity before that, we cannot make a withdrawal.

- Savings have lower risk & lower profit potential like our savings account, fixed deposits, etc. On the other hand, investments have higher risk & higher profit potential like investing in stocks, mutual funds, etc.

When to start investing? What are the steps in the investment process?

The earlier you begin investing, the more likely you are to gain the benefits of the power of compounding. Moreover, the best time to start investing is when you are starting out with your first job, with minimal debt obligations. It is also important for one to understand the flow of their money before they can begin investing it in assets. Following are the steps in the investment process–

- Assess your risk appetite- You should calculate your assets, liabilities, and most importantly your risk appetite to get a sense of our current financial situation.

- Evaluating investment objectives- You should create a detailed risk-return profile to understand the level of risk you are ready to undertake and the associated risk you can digest.

- Asset allocation- Diversification plays a key role in maximizing returns and minimizing risks as you should allocate funds to different asset classes as per our investment goals.

- Monitor portfolio performance- It is very important to keep monitoring your portfolio at regular intervals to ensure that it is taking you closer to achieving your financial goals.

What care should you take while investing?

- Evaluate your risk profile- Evaluate your risk profile because it will help you in selecting the right investment product.

- Pay off debts and maintain an emergency fund- Pay off your debts first and have an emergency fund to deal with any critical situation.

- Having a portfolio mix of investments- Have a portfolio with the right mix of investments to have better-risk-adjusted returns.

- Investing regularly- You should invest regularly with the same amount to take advantage of the power of compounding.

- Adequate insurance coverage- One should be adequately covered with insurance before investing.

What are various options available for investment?

A well-diversified portfolio is a balanced portfolio and it should not only give returns but also beat inflation.

Risk and return are directly related to each other. The more risk you are willing to take, there is chance of getting a higher return.

Whenever we are looking for investment plans, we should focus more on the risk-adjusted return.

Investment options are of two types:

1) Market-linked products

2) Fixed-income products

What is meant by Interest?

Interest is the cost of using the money of others. You pay interest when you borrow money (loan). You earn interest when you lend money (deposit).

Interest is the additional money that is necessary to pay to get money from someone. So, what does it cost to borrow money? The answer is more money.

It is expressed in terms of percentage of a loan or deposit and it is generally quoted annually.

There are two types of interest: simple and compound interest.

Simple interest: It is calculated on the principal amount at a flat rate basis. The principal is fixed over a period of time and interest is charged on that fixed amount till the end of the tenure.

Compound interest: In this type of interest calculation, the rate of interest is charged on the amount, which is the sum of principal and accrued interest. In simple words, it is the addition of interest to the principal amount. You can also look at it as an interest on interest.

How Does Inflation Affect Interest Rates?

Inflation is the increase in the general price level of goods and services in an economy and this will result in lower demand for goods and services.

The government uses interest rates to control inflation in the economy.

When inflation is to be reduced, interest rates are increased. The effect of a rise in interest rate is that the cost of loan rises and it makes loans expensive, which will lead to a lower supply of money.

On the other hand, when inflation decreases, the rate of interest also decreases which leads to the cost of loans getting inexpensive. This will lead to an increase in borrowing coupled with money supply. In such a scenario where demand of goods increases with supply remaining constant, price of goods and services increases which means rate of inflation increases.

What is Simple Interest?

By using Simple Interest, you can calculate the interest that is payable on a loan/principal amount. It is used in sectors like banking, finance, automobile, and so on.

Simple interest formula is given as:

SI = (P × R ×T) / 100

where,

SI = simple interest

P = principal

R = interest rate (in percentage)

T = time duration (in years)

What is Compound Interest?

Compound interest is the method where interest is calculated on the principal and the interest accumulated over the previous period. It is interest on interest.

The compound interest formula is given as:

A = P(1+R/n)nt

Where,

A = amount

P = principal

R = rate of interest

n = number of times interest is compounded per year

t = time (years)

Why 0% is not really 0% in EMI schemes?

EMIs relieve you from paying the huge upfront cost but it is important to remember that there is always a cost that you have to pay on these 0% EMI schemes.

Let’s have a look at how these schemes work:

What is Return?

Return is the gain or loss of an investment in a particular period which is expressed in terms of a percentage of the total amount.

The return on an investment can be calculated as follows:

Return = Amount Received - Amount Invested / Amount Invested

For example,

An investor purchases property A, which is valued at ₹50 lakhs. Two years later, the investor sells the property for ₹90 lakhs.

Return = (90,00,0000 – 50,00,000) / (50,00,000)

= 80%

What is the difference between return and interest?

Return: The percentage of loss & gain generated by an investment in return. A return is an internal measure to the investor.

Formula: Ending value of investment - Beginning value of investment / Beginning Value of investment x 100

Interest: The cost of borrowing or lending money is interest. Interest is an external measure that relates to the cost of getting money from a lender.

Simple interest formula is given:

SI = (P × R ×T) / 100

where

SI = simple interest

P = principal

R = interest rate (in percentage)

T = time duration (in years)

The compound interest formula is given as:

A = P(1+R/n)nt

Where,

A = amount

P = principal

R = rate of interest

n = number of times interest is compounded per year

t = time (years)

What are the types of Asset Classes?

The different types of asset classes are as follows:

Stocks: These are units that represent a portion of the ownership of a public company.

Fixed income: These are debt instruments that offer a fixed rate of return.

Real Estate: This refers to all types of property built upon and underground.

Commodity: The raw materials that are usually agricultural or naturally occurring, and are uniform in features.

What is a PAN Card and its importance?

Permanent Account Number (PAN) is a 10-digit alphanumeric identification number given by the income tax department to all taxpayers in India.

It is an important document for carrying out financial transactions like opening a savings bank account, applying for a debit/credit card, etc.

The importance of a PAN card is as follows:

- PAN details are required to open a new bank account

- You have to provide PAN details while investing money

- For filing tax returns

- To get a new phone connection

- While applying for a new credit/debit card as well as a loan

- Acts as a valid proof of identity

What are the types of bank accounts in India?

The types of bank accounts in India are:

- Savings account – Best suited for individual consumers, who need to store their money and not spend it as frequently as businesses.

- Current account – Best suited for businesses, with minimal limits on withdrawals and overdrawing facilities.

- Salary account – These accounts are opened for an employee on behalf of their employer. It is where an employee’s salary is credited.

- Fixed deposit account – A saving instrument where one can lock in a fixed sum of money for a period of time and receive interest on it.

- Recurring deposit account – A deposit account where one can deposit amounts periodically and earn interest similar to fixed deposits.

- NRI accounts – An account that is opened by a Non-Resident Indian (NRI) in a banking institute approved by the RBI.

How to select a suitable savings bank account?

There are few things that come under consideration while deciding the perfect savings account matching your requirements:

1. On the basis of your usage

Savings accounts should be chosen keeping in mind how you are going to use it.

2. Decide your priorities

You need to figure out your banking requirements like personalized banking or digital banking.

3. Never miss the disclaimers

While opening an account there are few terms and conditions which you should not overlook.

What is a Credit Rating?

Credit rating is a measurement of credit risks linked with a financial security or financial entity. Banks and lenders use credit ratings to analyze if you have the ability to repay a loan based on your income and past repayment records. It is usually expressed as a credit score and is one of the factors to determine whether to lend money.

For example, most businesses receive credit ratings expressed as letter grades (such as AAA, AA or A) from agencies such as Standard & Poor’s, while individuals receive a rating expressed as a credit score known as the CIBIL score.

What is a MAB (monthly average balance) and how does it affect you?

Monthly Average Balance or MAB is the minimum amount that is supposed to be maintained in your bank account at the end of each day of the month divided by the number of days in a month.

Let us look at an example.

Let us assume you have a balance of ₹15,000 on January 1 in your savings bank account. Assuming you withdrew ₹10,000 on January 5 but deposited ₹10,000 on January 20, here is how your MAB for the month will be calculated.

Jan 1 to Jan 4: EOD balance = ₹15,000*4 = ₹60, 000

Jan 5 to Jan 19: EOD balance = ₹5,000*15 = ₹75,000

Jan 20-Jan 31: EOD balance = ₹15,000*12 = ₹1,80,000

Total Balance = ₹60,000 + ₹75,000 + ₹1,80,000 = ₹315,000

Number of days in Jan (including bank holidays and working days) = 31

Final MAB = ₹3, 15,000/31 = ₹10,161.29

What is the maximum EMI I can service?

The EMI of your loans will be determined on the basis of the tenure of repayment you select.

Banks follow a general policy of not considering more than 35-40 % of your net pay as EMI, inclusive of your repayment obligations on other loans, if any.

The basic criteria for deciding EMI is based on the percentage of the salary of an individual.

Consider these two cases:

Case I:

Mr A earns ₹20,000 per month. If banks take away 40 % of his salary towards EMI he will be left with only ₹12,000.

Case II:

Mr B earns ₹50,000 per month. If he sets aside 40 % of his salary, he will still have ₹30,000 to meet his monthly expenses.

What is a credit card and how to use it?

A credit card allows you to make purchases by borrowing money from the credit card issuer up to a pre-defined limit. It is like a short-term loan.

You should use your credit card in the following ways:

- Spend only when you must and maintain your budget.

- Pay your bill on time.

- Read your Credit Card brochure about the benefits it offers and the reward program.

- Repayment method should be selected smartly.

- Minimize risk by using your card at trusted merchants.

- Spend within your credit limit.

- Do not close credit card accounts randomly.

What is credit score (CIBIL score) and importance of credit history?

A credit score is a 3-digit number that shows the probability of you repaying your loans. It is used by banks and lenders to assess the risk they are taking by lending money to you. It ranges from 300 to 850.

Your credit history is the first thing that is checked by banks and lenders, whenever you apply for a loan. Credit history allows banks and lenders to determine your ability to repay the loan on time by checking when and where you applied for credit, whom you borrowed money from, and whom you still owe. Thus, the major importance of having a credit history is your risk assessment.

Pay off credit card debt or Invest?

Credit card debt is the most expensive form of borrowing.

When you purchase using your credit card, the interest charged is 2-3% a month (or 24-36% a year). Credit card companies charge high-interest rates to protect themselves if you accumulate a lot of debt or you never pay them back.

Hence, they come with high-interest rates and a small minimum balance that needs to be paid every month, making you unable to save.

Therefore, paying off the credit card is a better decision than investing the same amount as a decent investment would fetch you 12-18% returns but beating a 36% interest rate with this investment could be very difficult.

Meaning & usage of NEFT / RTGS / IMPS

NEFT- National Electronic Funds Transfer (NEFT) is a national payment system that helps us to transfer money from one bank account to another. It is a mode of online money transfer that was introduced by the Reserve Bank of India (RBI). In order to transfer money online, your bank account must be NEFT- enabled.

- TIMINGS: Fund transfers can be made on a 24x7 basis. NEFT fund transfer can be made from ₹1.

- TRANSACTION LIMIT: RBI has not set any maximum limit for online transfers. Banks, however, can set their own limits on the bank account holders.

RTGS- Real Time Gross Settlement (RTGS) is the method of transferring large amounts of money from one bank account to another.

‘Real Time’ means the instructions are processed whenever it is received.

‘Gross Settlement’ means that the instruction of fund transfer takes place individually.

- TIMINGS: Earlier fund transfer using RTGS mode is not available 24x7. The window is available to banks from 7 a.m. to 6 p.m. on a working day, for settlement at the RBI end. Now, RBI has announced that from Dec 2020, RTGS will be available 24x7.

- TRANSACTION LIMIT: As per RBI, the minimum amount that can be transferred is ₹2 lakhs and there is no maximum limit.

IMPS- Immediate Payment Service (IMPS) is a real-time online payment mode to transfer money from one bank account to another. IMPS is the mix of both RTGS and NEFT.

- TIMINGS: Fund transfers can be made on a 24x7 basis.

- TRANSACTION LIMIT: IMPS can be used to transfer a maximum amount up to ₹2 lakhs, instantly.

What is a Bond?

A bond is a type of debt that borrowers take from individual investors for a specified time period. It is a fixed-income security that signifies a loan given by an investor to organizations like companies, governments, municipalities and other entities.

It helps organizations to raise funds and meet their capital requirements. You can purchase bonds from the primary markets at face value or principal. Investing in bonds gives you the legal and monetary rights to an organization's debt fund. The borrowers are liable to return back the entire face value of bonds after the term period expires.

What is a Derivative?

A derivative is a financial contract between two parties that derives its value from an underlying asset. This means that they possess no value of their own, but are dependent on the asset to which they are linked.

The buyer enters into an agreement with the seller to purchase the asset on a specific date at a fixed price.

In some cases, the seller does not necessarily have to own the asset but can give the necessary amount to the buyer to purchase it at the prevailing price. The seller can also give another derivative contract that balances the value of the previous one.

Derivatives are often used for stocks, bonds, currency, commodities, and interest rates.

What is a Mutual Fund?

A mutual fund is a professionally managed investment scheme that is run by an asset management company (AMC). Mutual funds help small investors to take advantage of professionally-managed, diversified portfolios of equities, bonds, and other securities, which are generally difficult to create with small amounts of capital.

As the name specifies, when you buy a mutual fund, your money is mutually pooled along with other investors. You can put money into a mutual fund by purchasing units or shares of the fund, which basically represents your proportion of holdings in a particular scheme. Investors share the profits and losses of the fund in accordance with their shareholding in the fund.

Public Provident Fund (PPF)

Public Provident Fund (PPF) is a long-term investment option that is backed by the Government. Hence, it is a risk-free investment plan.

You can use a PPF calculator to estimate your returns and plan your investments more effectively.

Some of its basic features include –

Employees Provident Fund (EPF)

Employees Provident Fund (EPF) is a savings scheme where an employee contributes 12% of their monthly salary towards the fund, and the employer matches this contribution. Over time, this builds a significant corpus with interest, which the employee receives as a lump sum upon retirement. To estimate your returns and plan better, you can use an EPF calculator to get a clear picture of your future savings.

Some of its basic features include–

National Savings Certificate (NSC)

National Savings Certificate (NSC) is a low-risk investment plan that can be purchased from any post office and is backed by the Government of India. It offers a fixed return and is generally used for tax-saving purposes.

Some of its basic features include–

Post Office Monthly Income Scheme (PO MIS)

Post-Office Monthly Income Scheme (POMIS) is one of the best schemes for monthly income. It is regulated by Post Offices and backed by the Government which allows investors to save a specific amount every month.

Senior Citizen Saving Scheme (SCSS)

The Senior Citizen Savings Scheme (SCSS) is a government-backed retirement benefits program. Senior citizens in India can invest a lump sum in the scheme, either individually or jointly, to get regular income as well as tax benefits. It is a saving scheme offered by the Post Office.

Feature | Senior Citizen Savings Scheme (SCSS) |

Investment Type | Fixed-income deposit scheme |

Eligibility | Individuals aged 60 years or above (or 55 years or above for retired defence personnel and retired government employees) |

Minimum Investment | Rs. 1,000 |

Maximum Investment | Rs. 30 lakh |

Interest Rate (as of July 4, 2024) | 7.4% p.a. (interest reviewed quarterly) |

Maturity Period | 5 years (extendable for 3 more years) |

Liquidity | Low, premature closure with the penalty |

Risk | Low (backed by the Government of India) |

Under Section 80C of the Income Tax Act, 1961, individuals are eligible for tax deductions on investments up to Rs.1.5 lakh. If the total interest in all SCSS accounts exceeds Rs.50,000 p.a., TDS will be deducted.

Kisan Vikas Patra (KVP)

Kisan Vikas Patra (KVP) is a savings certificate scheme offered by the Government of India, designed to encourage long-term financial discipline among small savers. It is especially popular in rural and semi-urban areas.

Here are some of its basic features–

Feature Kisan Vikas Patra (KVP) Benefit Guaranteed returns, doubles investment at maturity Investment Type Fixed-income scheme Minimum Investment Rs. 1,000 Investment in multiples of Rs. 100 Maximum Investment No maximum limit Interest Rate (as of Q1 FY 2024-2025) 7.5% compounded annually Maturity Period 115 months (approx. 9.5 years) Tax on Interest Yes, taxable as per the income tax slab Tax Deduction at Source (TDS) on withdrawal No Liquidity Low, Premature closure allowed only in exceptional cases Risk Low (backed by the Government of India)

Company Fixed Deposits (FDs)

Company Fixed Deposits (FDs) are term deposits offered by non-banking financial companies (NBFCs) and corporates. They work similarly to bank fixed deposits but typically offer higher interest rates. However, they also come with higher risks compared to bank FDs.

Company Name Credit Rating Regular Deposit Cumulative Option* ROI (p.a.) (As on ) Additional for Senior Citizens 1 Yr 2 Yr 3 Yr 4 Yr 5 Yr Senior Citizen Mahindra Finance Ltd CRISIL- FAAA & ICRA - MAAA 7.50% 7.80% 8.10% 8.10% 8.10% 0.25% Bajaj Finance Ltd CRISIL- FAAA & ICRA - MAAA 7.40% 7.50% 7.80% 8.10% 8.10% 0.25% Shriram Transport CRISIL- FAA & ICRA - MAA 7.85% 8.15% 8.70% 8.75% 8.80% 0.50% ICICI Home Finance CRISIL- FAAA & ICRA - MAAA 7.25% 7.55% 7.65% 7.60% 7.50% 0.25%

RBI Savings Bonds

It is a low-risk investment scheme for investors who want protection and a return of capital at the end of the tenure (7 years). You have to invest a minimum of ₹1000 and there is no limit to the upper side.

These bonds were launched by the Reserve Bank of India (RBI) in August 2020. The interest rate offered by the bonds is not fixed and is linked to the current prevailing interest rate, because of which, these bonds would come under the category of floating interest rate securities.

Capital Gain Bonds or 54 EC Bonds

They are one of the best financial instruments for investors earning long-term capital gain tax and would like to get tax exemptions on these gains under section 54EC of the Income Tax Act. The maximum limit for investment is Rs 50 lakhs. These bonds constitute bonds from the National Highway Authority of India (NHAI) and the Rural Electrification Corporation (REC). An important thing to remember is that, to get the required tax benefits, one must invest the capital gain they got from the sale of a property.

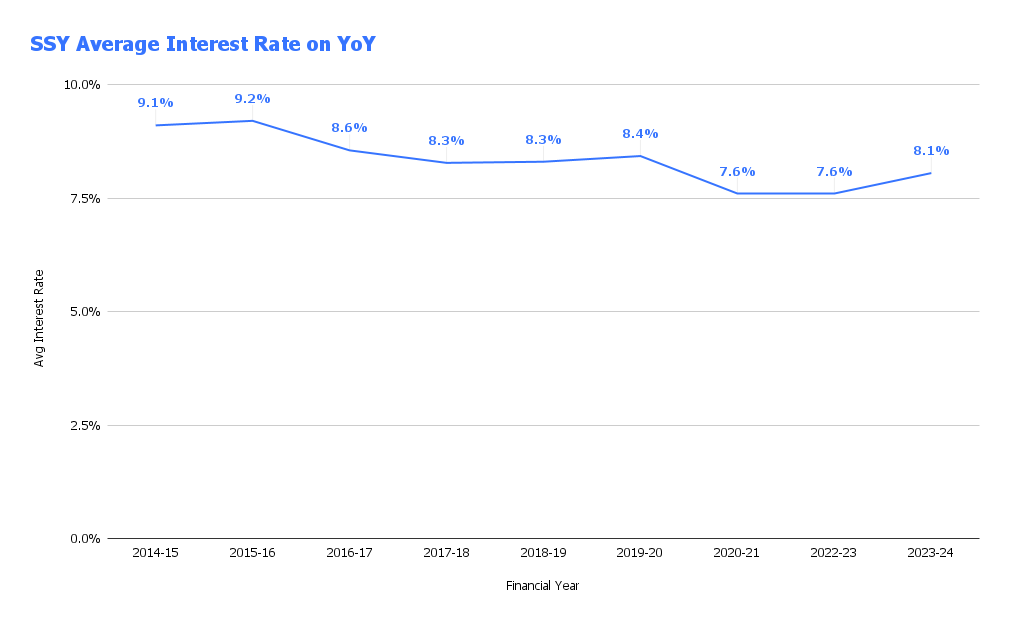

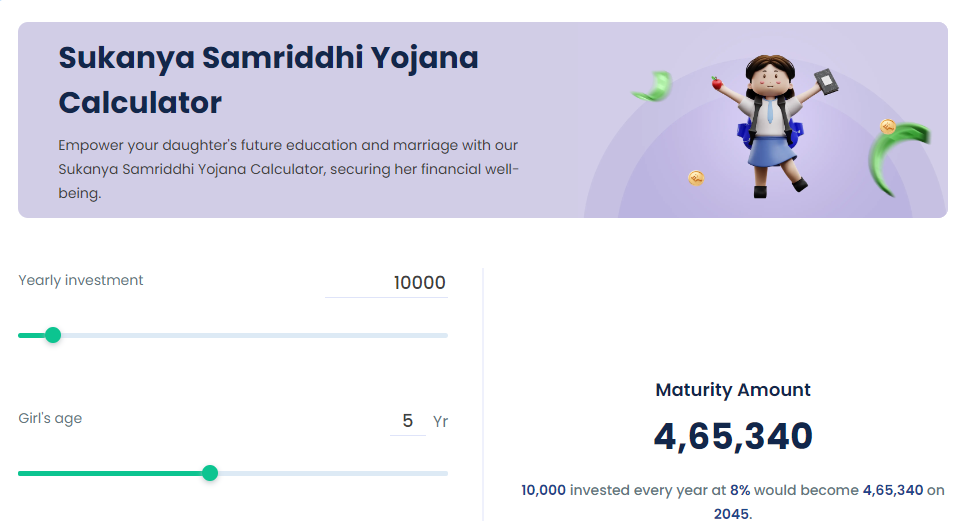

Sukanya Samriddhi Scheme (SSS)

Sukanya Samridhi Yojana is a small savings scheme launched by the Government as a part of their ‘Beti Bachao, Beti Padhao’ campaign.

Overview of SSS | |

Age Limit | 0-10 Years |

Investment Amount | ₹250 - ₹1,50,000 |

Maximum Account can be opened | 2 |

Maturity Duration | 21 Years |

Contributions to SSY accounts not only secure your child's future but also offer significant tax benefits.

Under Section 80C, you can claim deductions up to Rs. 1.5 lakh annually. Moreover, the interest earned and withdrawals are completely tax-free, making it a smart financial move.

Here’s the chart showing the average interest rate of SSY on a YoY basis

To calculate the maturity amount, check out the Sukanya Samriddhi Yojana Calculator.

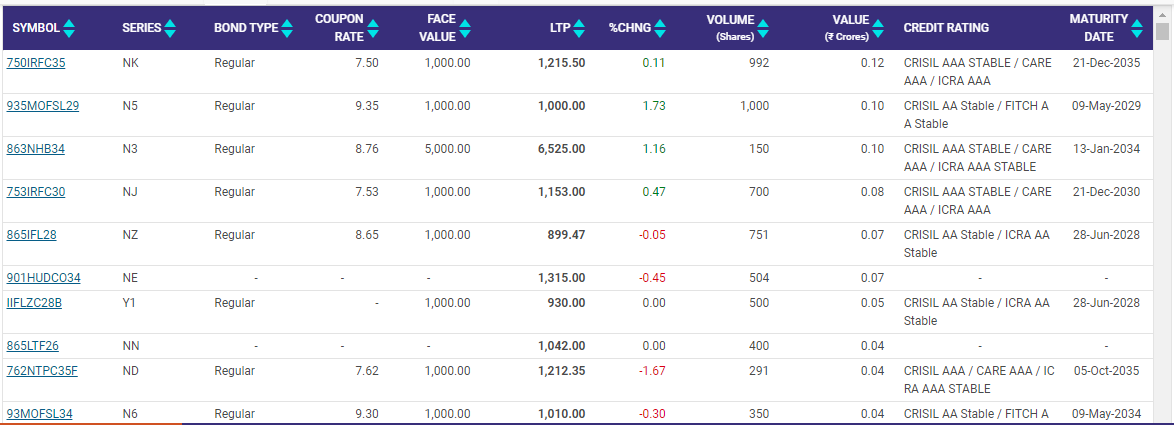

Non-convertible Debentures (NCDs)

A non-convertible debenture is a way to raise long-term capital for companies through public issues. Since these debentures lack the option of convertibility, they usually offer higher interest rates compared to convertible debentures.NCDs have a fixed maturity date with higher returns, liquidity, low risk, and tax benefits.

There are two types of NCDs –

- Secured NCDs are backed by the assets of the company. If the company cannot pay, the investors can claim their debt through the liquidation of assets.

- Unsecured NCDs are riskier as they are not backed by any asset of the company.

Coupon Bearing bonds

A coupon bearing bond, also known as a coupon bond or bearer bond, is a type of debt security that pays periodic interest payments to the holder. These bonds have detachable coupons attached to the certificate, which represent the individual interest payments.

Here's how it works:

Issuance: A company or government issues a coupon bond with a specific face value, interest rate (coupon rate), and maturity date.

Interest Payments: The bond certificate has detachable coupons, each representing an interest payment for a specific period (usually semi-annual).

Collecting Interest: To collect interest, the bondholder detaches the appropriate coupon from the certificate and presents it to the issuer's paying agent on the payment date. The agent verifies the coupon's authenticity and makes the interest payment to the bearer.

Maturity: When the bond reaches its maturity date, the bondholder can redeem the certificate for its face value.

To get comprehensive data on Indian Corporate Bonds & Debenture, you can check out the NSDL India Bond Info.

Tax-Free Bonds

Tax-free bonds are issued by the Government to raise long-term funds, usually for a specific purpose. An example of these includes municipal bonds. It is a low-risk investment option that offers a fixed rate of interest. The most attractive benefit is the tax exemption as per Section 10 of the Income Tax Act of India, 1961. It has a long-term maturity of 10 years and more.

Issuer | Coupon rate (Interest rate) | Maturity Date | Yield to Maturity (%) |

National Highways Authority of India (NHAI) Tax-Free Bonds | 8.75 | 05-Feb-2029 | 5.48 |

National Housing Bank | 9.1 | 16-Nov-2033 | 5.01 |

National Thermal Power Corporation (NTPC) Tax-Free Bonds | 8.91 | 16-Dec-2033 | 5.6 |

Rural Electrification Corporation (REC) Tax-Free Bonds | 8.71 | 24-Sep-2028 | 5.49 |

Housing and Urban Development Corporation (HUDCO) Tax-Free Bonds | 7.64 | 8-Feb-2032 | 5.7 |

Indian Railways Finance Corporation (IRFC) Tax-Free Bonds | 8.63 | 26-March-2029 | 5.11 |

Power Finance Corporation (PFC) Tax-Free Bonds | 8.67 | 16-Nov-2033 | 5.2 |

For real-time updates on the bond market, you can visit the NSE Website.

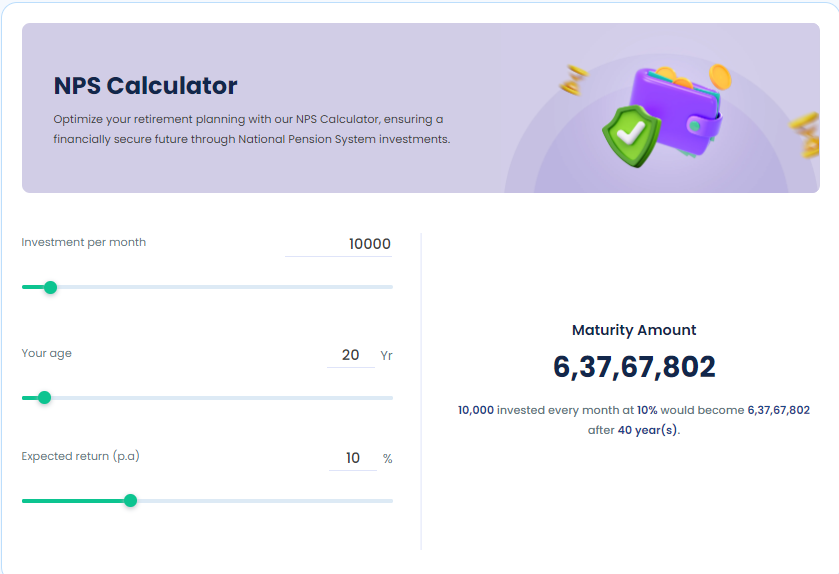

New Pension Scheme (NPS)

The National Pension System (NPS) was launched on 1 January 2004 with the objective of providing retirement income to all citizens. It is a voluntary, defined contribution retirement savings scheme designed to enable the systematic savings of individuals during their working life.

The NPS scheme aims to provide old-age income security to all Indian citizens, particularly targeting the workforce in the unorganized sector. It is regulated by the Pension Fund Regulatory and Development Authority (PFRDA).

Eligibility:

Open to all citizens of India aged between 18 and 65.

Available to both salaried and self-employed individuals.

Account Types:

Tier I Account: This is the primary pension account with restrictions on withdrawals. It is mandatory and offers tax benefits.

Tier II Account: This is a voluntary savings account without withdrawal restrictions, primarily used for investment purposes. It doesn't offer additional tax benefits like the Tier I account.

Tax Benefits:

Contributions up to INR 1.5 lakh are eligible for tax deduction under Section 80C.

Additional deduction of up to INR 50,000 under Section 80CCD(1B).

Employer contributions up to 10% of salary (basic + DA) are deductible under Section 80CCD(2).

To calculate the maturity amount use our NPS Calculator

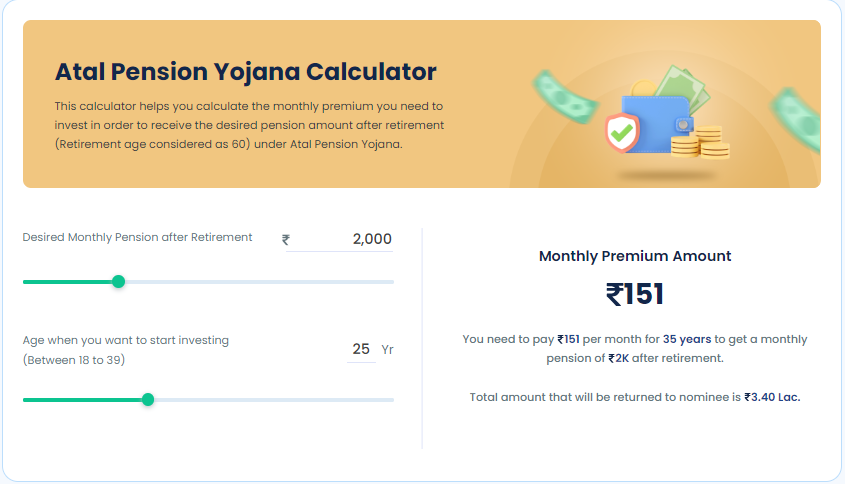

Atal Pension Yojana (APY)

Atal Pension Yojana (APY) is a pension scheme introduced by the Government of India specifically for the unorganised sector. Individuals in the organised sector who do not get pension benefits can also invest in the scheme.

Atal Pension Yojana Eligibility

The following are the criteria to be eligible for the Atal Pension Yojana benefits:

Must be an Indian citizen.

Between the ages of 18 and 40.

Should put in at least 20 years' contributions

To link your bank account to your Aadhar.

A working mobile phone number

Tax exemption is also available under Section 80CCD of the Income Tax Act, 1961.

To calculate the monthly premium amount using the Atal Pension Yojna Calculator, click here

What is meant by a Stock Exchange?

A stock exchange is a place where buyers and sellers meet to trade financial instruments like stocks, bonds and commodities while following SEBI’s well-defined guidelines.

Two popular stock exchanges in India are:

- Bombay Stock Exchange (BSE)

- National Stock Exchange (NSE)

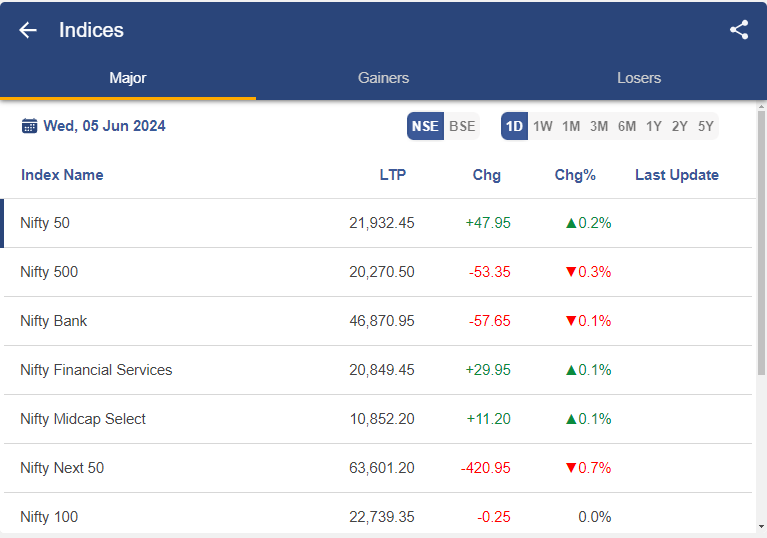

What is an Index?

An index in a measurement of the performance of a group of stocks, such as a list of publicly traded companies and their stock prices. It helps us to compare the performance of any one stock against the overall market. An index acts as a barometer and it acts as a benchmark. So it gives an idea of the broader market or sector.

To track the performance of Indices, visit StockEdge

What is a Depository?

A Depository Participant is an entity which is responsible for maintenance of ownership records and helps an investor to buy and sell securities in a paperless form. Depositories work as an intermediary between listed companies and shareholders. The Securities and Exchange Board of India (SEBI) is responsible for the registration, regulation and inspection of the depository.

The two depositories in India are:

- National Securities Depository Limited (NSDL)

- Central Depository Services Limited (CDSL)

What is Dematerialization (DEMAT)?

Dematerialization is the process of allowing investors to convert their physical shares into digital format and they are held in a Demat account. Dematerialization eliminates the risks like certificate forgeries, loss of important share certificates, and consequent delays in certificate transfers.

What is an ASBA facility?

ASBA (Application Supported by Blocked Amount) is an application that can be used by an investor to apply in IPOs/FPOs/Rights shares and acts as an authorisation to block the application money in the bank account for subscribing to an issue. When applied using the ASBA form, your money will be debited from the bank account only if shares are allotted to you. ASBA facility can be used when any company comes up with any type of issue i.e. public and rights.

What is meant by Securities?

Securities are financial instruments that can be bought and sold. They are investments that represent debt or ownership or the legal right to acquire or sell an ownership interest. Some examples of securities include–

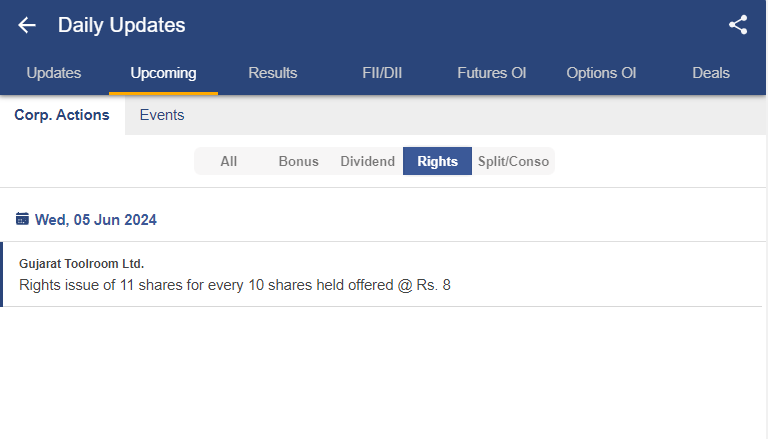

Rights Issue Shares

When a company wants to raise additional capital, they go for a rights issue. It is an offer to existing shareholders to buy additional shares of the company. New shares are generally offered at a discounted price.

To track the right issue of shares, check below in StockEdge.

Bull and Bear markets

A bull market is a phrase of several months or years during which stock prices continue to rise. It indicates that the economy is in good shape and the unemployment rates are generally low which give investors more confidence.

A bear market is a phrase of several months or years during which stock prices continue to fall. It indicates a slowing economy and rising unemployment rates.

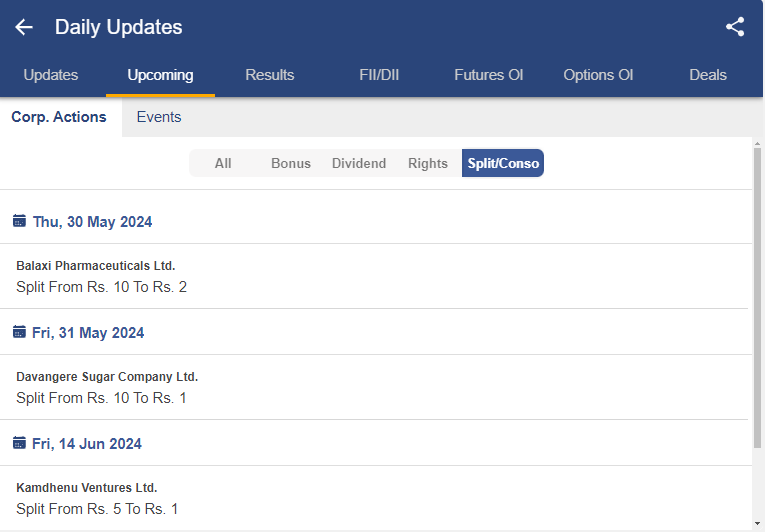

Stock Split & Bonus Shares

Stock Split and Bonus Shares are both corporate actions that companies undertake to manage their share capital and make their stock more accessible or attractive to investors.

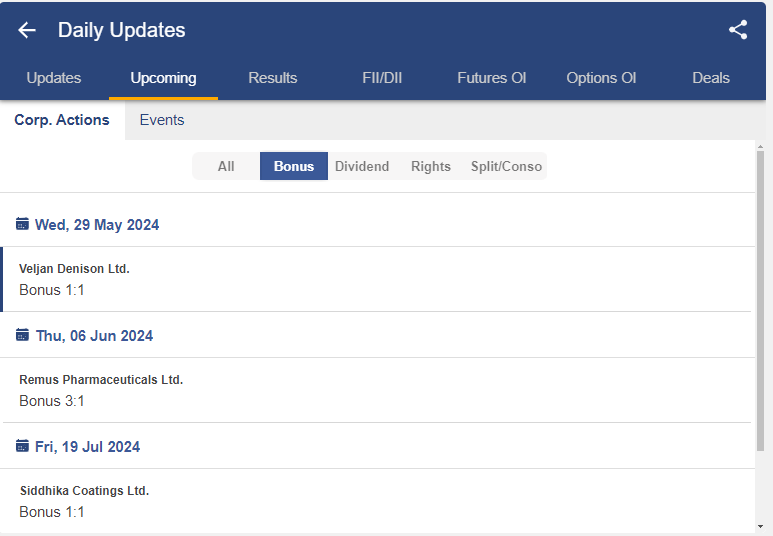

What is Bonus Share?

Bonus shares are additional shares that a company gives to its shareholders without any cost. It is the share of profits that are not given out in the form of dividends but are converted into free shares.

For example, a Bonus of 4:1 means 4 extra shares for every share held by you.

Check out StockEdge to track which companies have announced Bonus Shares.

What is Stock Split?

A stock split increases the number of shares of a company, but the market capitalization remains the same. Due to an increase in the number of shares, the price per share decreases.

For example, a 4-for-1 stock split means you will get an additional 3 shares for every share held.

What is the Auction Process?

Before understanding what auction means, let’s understand what is pay-in & what is pay-out day?

Pay-in is the day when your broker collects the securities from your demat account and transfers them to the exchange and clearing member. This happens when you sell a security. On the other hand, pay-out is the day when the clearing member transfers the securities to the broker. The broker then transfers those securities to your demat account. This happens when you buy a security.

An auction process is a mechanism where an exchange auctions the investor’s stock holding when the person has sold the stock but is unable to deliver it within a stipulated time period. An auction can be a live, online, or sealed bid auction.

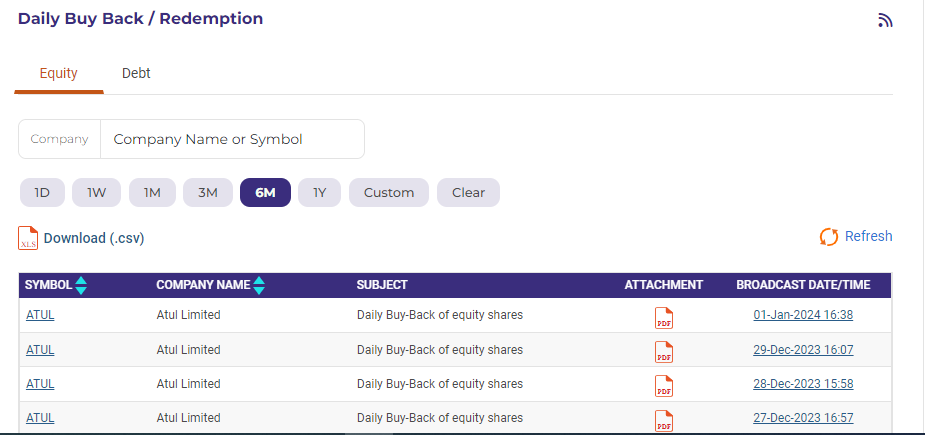

What is Buyback of shares?

A buyback of shares, also known as a share repurchase, is a corporate action in which a company buys back its own shares from the existing shareholders. This can be done through the open market or through a tender offer.

Visit the NSE website to find out which companies have announced buyback shares.

What are the Key Dividend Dates?

Dividends are the way by which a company returns back a part of its profits to shareholders. There are 4 important dates to keep in mind while holding a dividend-paying stock:

Declaration Date: The declaration date is the date when the board of directors announces and approves the payment of a dividend.

Ex-Dividend Date: This is the cutoff date to be eligible to receive the declared dividend. If you purchase the stock on or after this date, you will not receive the next dividend. Typically, the ex-dividend date is set one business day before the record date.

Record Date: The record date, also known as the date of record, is the date on which the investor must be listed on the company's books in order to receive a dividend.

Payment Date: This is the date on which the company distributes the dividend to the shareholders. It’s the day you actually receive the dividend in your account.

Where to find the stocks related information?

It is important for investors to stay updated regarding stock-related information and current market scenarios. The stock market is a dynamic place. Here is the best site for stock market news and reliable information:

NSE India (www.nseindia.com)

BSE India (www.bseindia.com)

StockEdge (www.stockedge.com)

Moneycontrol (www.moneycontrol.com)

Economic times (economictimes.indiatimes.com)

Bloomberg (www.bloomberg.com)

CNBC (www.cnbctv18.com)

Investing (in.investing.com)

Factors Affecting Share Prices in the Stock Market

There are various factors that affect the stock price. Here are some of them:

Supply and Demand: One of the most significant factors influencing the stock market is the imbalance between supply and demand, which causes stock prices to rise or fall. When the demand for a particular stock exceeds its supply, indicating more buyers than sellers, the price tends to rise.

Fundamental Factors: Financial health indicators such as earnings, revenue growth, profit margins, and cash flow are critical. Strong performance typically attracts investors, increasing demand and driving up share prices.

Economic Conditions: The state of a country’s economy and global economic developments significantly impact share prices. A strong economy usually boosts investor confidence, leading to higher stock prices.

Government Policies: Policies that affect corporate taxes, industry regulations, and economic incentives can significantly impact share prices. Favourable policies can stimulate growth and investment, driving up stock prices.

Political Climate: Political stability tends to foster investor confidence, while political uncertainty or turmoil can increase risk perceptions, leading to market volatility.

Market Sentiment: Investor psychology plays a significant role. Bullish sentiment (optimism) generally leads to rising share prices, while bearish sentiment (pessimism) can lead to falling prices.

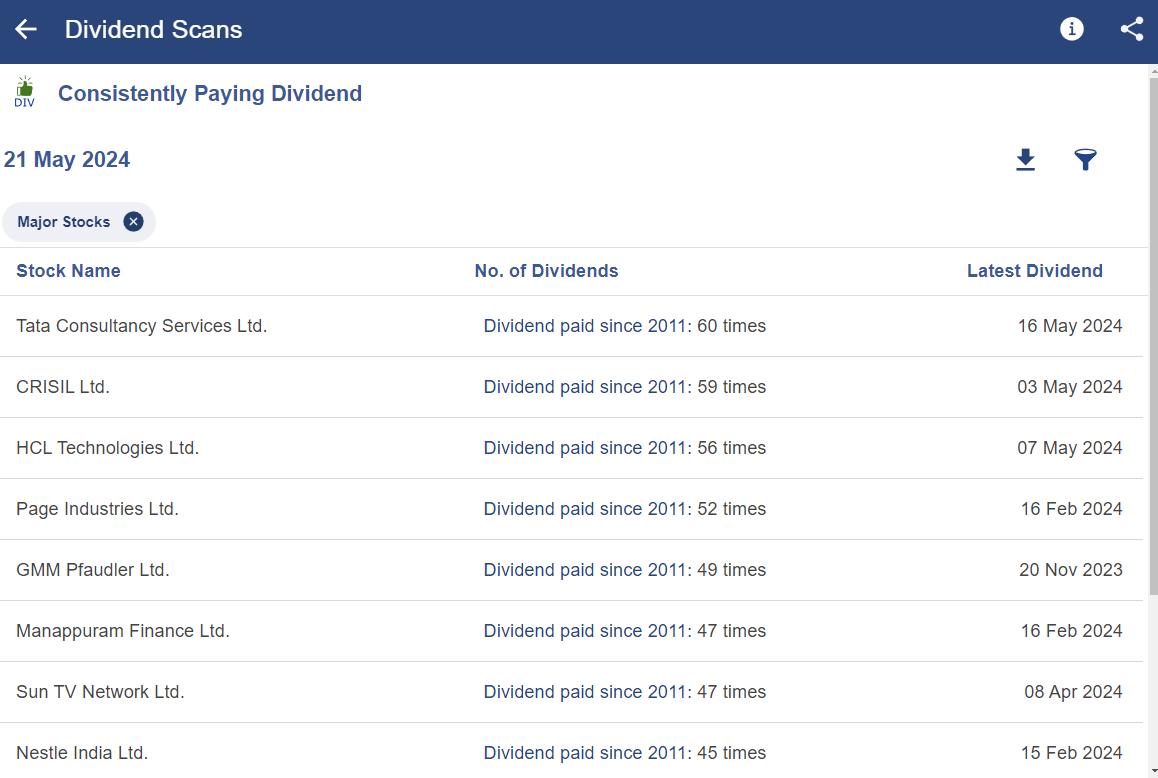

Dividend & Dividend yield

A dividend is a distribution of profits by a corporation to its shareholders. It is a portion of the company's earnings that is returned to investors as a reward for their ownership of the company's stock. Dividends are typically paid out in cash, but they can also be in the form of additional shares of stock or other property.

Dividends are usually declared by the company's board of directors and are distributed on a regular basis, such as quarterly or annually. The amount of the dividend per share is determined by the company's profitability and financial position, as well as any other factors deemed relevant by the board of directors.

To track the dividend payout, click below StockEdge.

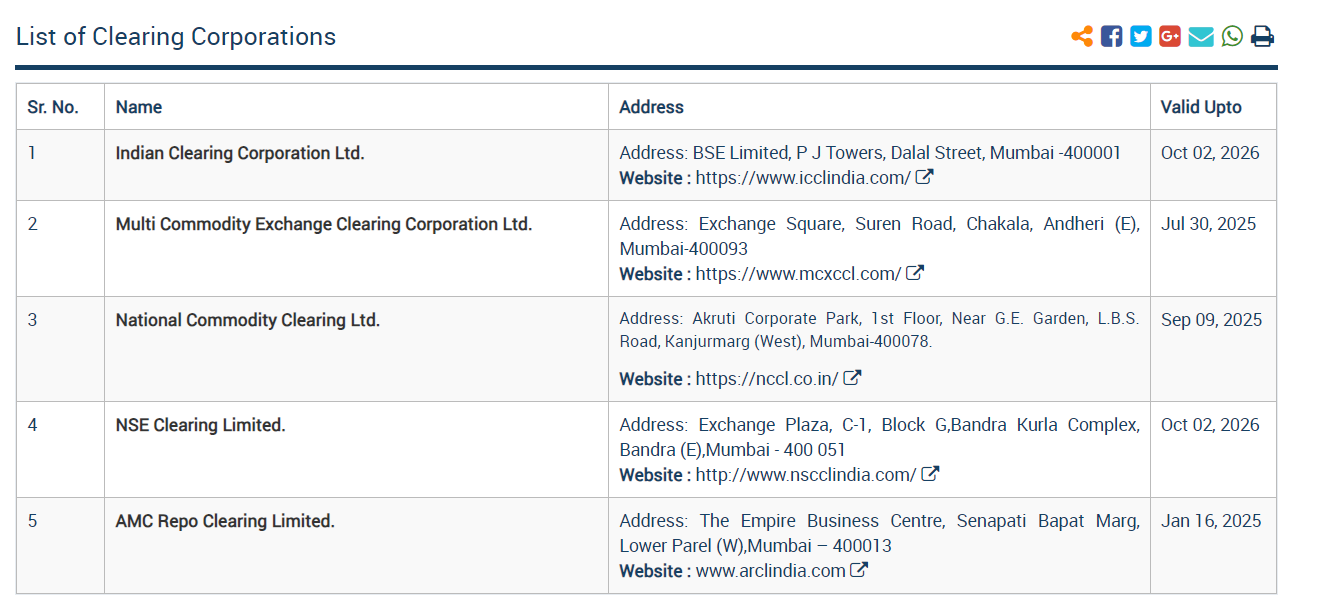

What is a Clearing Corporation?

A clearing corporation, also known as a clearing house or clearing firm, is associated with a stock exchange and is responsible for the confirmation, delivery, and settlement of transactions in the stock market.

This process is handled by the National Securities Clearing Corporation Limited (NSCCL), a non-profit organization set up by the Securities and Exchange Board of India (SEBI) in 1995. NSCCL's job is to make sure everything goes smoothly when shares are bought and sold.

Here’s the list of Clearing Corporation

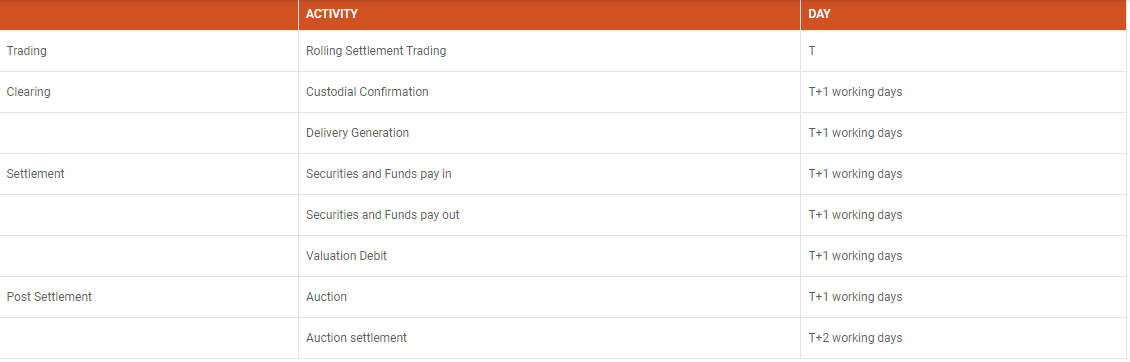

What is Rolling Settlement?

Rolling settlement is the process of settling trades every day based on the particular date on which the original trade was placed.

Currently, NSE Clearing adopts a T+1/T+0 rolling settlement cycle. For all trades made on the T day, NSE Clearing determines each member's provisional cumulative obligations and electronically communicates the information to Clearing Members (CMs). All trades executed on a specific trading date are settled on a predetermined settlement day, i.e. T+1/T+0.

In case of short deliveries on the T+1 day in the regular segment, NSE Clearing conducts a buy-in auction on the T+1 day itself, and settlement is completed on the T+2 day.

Check out the NSE settlement cycle for rolling settlement in the stock market:

How does one decide to buy and sell any equity share?

Deciding when to buy a stock and when to sell a stock depends on fundamental and technical analysis. Let’s explore the key parameters:

Fundamental analysis: Evaluate the company’s financial position to determine its investment potential. Buy the stock if the company consistently shows strong financial health, indicating robust earnings reports, a strong balance sheet, positive cash flow, and favourable valuation ratios. Conversely, sell the stock if the company shows financial instability.

Technical analysis: Identifying optimal entry and exit points is crucial in technical analysis for effective trading decisions. When the stock shows upward trends, breaks through resistance levels, or produces bullish chart patterns, these indicate optimal entry levels and vice versa.

To check out the entry and exit levels of the stocks, you can check the Trading Strategies section at StockEdge

What are the various types of the risks once I start trading?

Most traders prioritize risk management very low on their list of priorities. However, profitable trading is not possible without adequate knowledge of risk management. To become a successful and professional trader, a trader must learn how to control risk, size positions, develop discipline, and set orders correctly. In this module, you will learn the types of risk involved in trading and how to manage them.

Types of Risk in Trading

Systematic Risk: Systematic risk, also known as market risk, is the uncertainty that affects multiple investments and cannot be mitigated through diversification. It is typically caused by macroeconomic variables such as inflation, currency fluctuations, geopolitical tensions, and environmental events.

Unsystematic Risk: Unsystematic risk, on the other hand, refers to a specific investment or industry sector and can include changes in management, legal disputes, and other factors.

Key points for managing risk on trading

Position Sizing: Determine the appropriate size of each trade based on your risk tolerance and the volatility of the asset.

Stop Loss Orders: Set stop-loss orders to automatically exit trades if the price moves against you beyond a predefined threshold.

Diversification: Diversify your risk across different assets, sectors, or trading strategies to reduce the impact of any single loss.

Trade with Discipline: Follow your trading plan rigorously and avoid impulsive or emotionally driven decisions.

What is an Overvalued Stock or an Undervalued Stock?

Determining the value of a stock involves assessing its intrinsic worth based on various factors such as the company's financial health, growth prospects, industry trends, and market conditions.

Identifying overvalued and undervalued stocks requires an in-depth analysis of their intrinsic value. While the intricacies of intrinsic value will be discussed later, let us first focus on the most important parameters for evaluating the stock value.

A stock's value is often determined using a combination of fundamental analysis, technical analysis, and market sentiment. Here is a breakdown of each approach.

Fundamental analysis: This approach focuses on determining a stock's intrinsic value by analyzing its financial performance. Investors frequently use valuation ratios that measure a company's financial strength to its market value. Click here

Technical Analysis: In technical analysis, indicators such as the Relative Strength Index (RSI) and Bollinger Bands have predefined overbought and oversold conditions. Overbought reflects the overvalued stock and oversold indicates undervalued stocks. Click here

- Sentiment Analysis: Market sentiment refers to the overall attitude or mood of investors towards a particular stock, sector, or the market as a whole. Using market breadth, you will determine the level of participation and conviction behind market moves, allowing for informed decisions. Click here

In the coming chapters, we will dive into more detail about these topics. You can check out the course on Stock Valuation Made Easy to understand how to find stock is undervalued or overvalued.

Explain the terms -selling short and Margin Trading

Selling a stock when the price is high and buying when the price drops down is called short selling. Here you buy or sell a stock which practically doesn’t belong to you. Whenever a short selling is done you need to place an MIS (Margin Intraday Settlement) order. However, short selling needs to be covered within the same day, i.e., intraday settlement.

When an investor wants to buy more stock than what they can afford, then end up borrowing funds from a broker to purchase a stock. This practice is called margin trading. Margin money increases the purchasing power of the investor. The broker lends money on interest and keeps the share as the collateral. There are two types of margin trading: intraday and delivery.

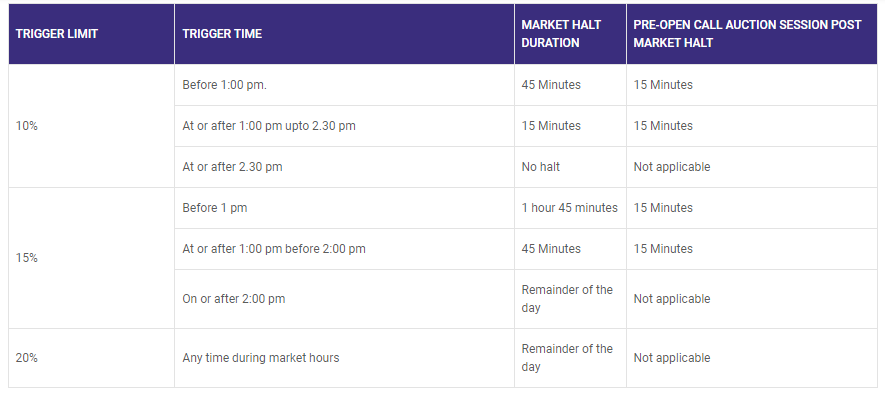

What are Circuit filters & trading bands

Stocks and indices act to buy and sell trades in the market, but unexpected news, whether positive or negative, can cause significant price movements, increasing market volatility. Such volatility can be harmful to retail investors, who frequently react late to news and may struggle to execute deals at favourable pricing. To reduce volatility and protect investors, SEBI implemented circuit limits and price ranges in the market.

So, before understanding the circuit limits, let’s understand trading bands which are also known as price bands. Stock exchanges set the range of stock price movements during trading hours, beyond which trading is temporarily halted or restricted.

Circuit filters typically consist of upper and lower price limits within which traders can trade during a single trading session. These limits are usually based on the previous day's closing price and once triggered, they halt trading temporarily (circuit breaker) or limit price movements to prevent extreme volatility.

Price limits are imposed by regulatory authorities SEBI (Securities and Exchange Board of India) to prevent excessive price movements in indices or equities with futures and options (F&O) contracts. This range can be from 2% to 20%, depending on the volume, liquidity, and kind of stock.

In the case of Indices, the duration of the market halt and pre-open session are as follows:

What is Insider Trading?

The concept of insider trading is similar to having prior access to the answers before taking a test. Let us understand the definition of insider trading.

Insider Trading Meaning

Insider trading is an unfair practice where insiders, such as key employees or executives of teh company, who have access to valuable information about the company, take undue advantage to profit from trading the company’s stocks. SEBI highly discourages insider trading to facilitate fair trading in the market.

In India, insider trading has serious implications. Traders and intermediaries must make themselves aware of the regulations involving price sensitive information. Price sensitive information includes that which is revealed to only a set of people, the usage of which can give traders an unlawful upper hand while trading in the market.

To check out insider deals, you can check the Daily update section at StockEdge

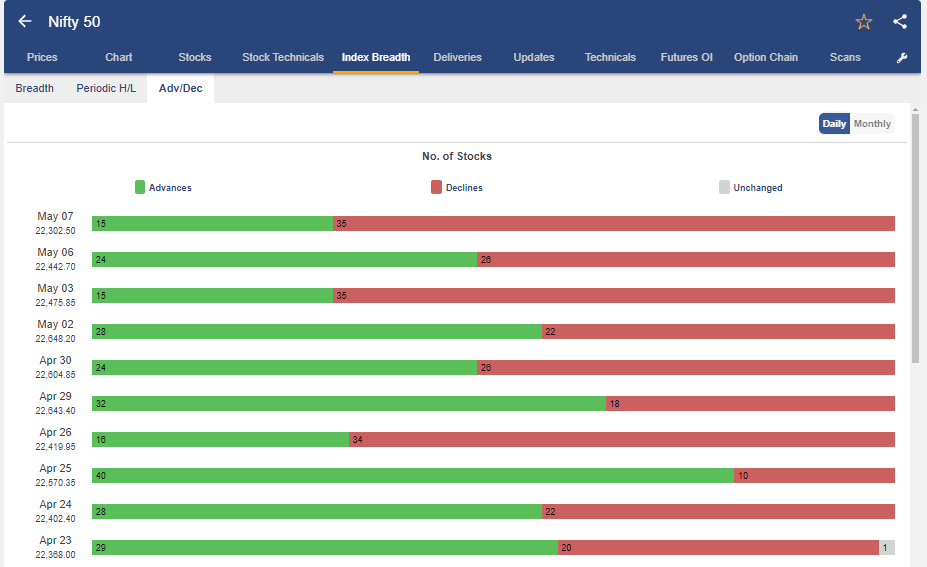

What are advances and declines?

Advance and decline in the stock market are important indicators that provide insights into the overall share market sentiment and trend.

Stocks that show strong market sentiment are referred to as advances, as their prices have increased from the day's prior closing price.

Declines indicate bearish sentiment in the market, as their prices have fallen from the day's prior closing price.

How to Interpret Advance and Decline in share market?

If advances > declines - market breadth is bullish (GREEN)

If advances < declines - market breadth is bearish (RED)

To track market breadth, and gauge market sentiments, check below in StockEdge

How much equity should I have? OR What should your asset allocation be?

In this session, you will learn about the optimal asset allocation, with a focus on equity allocation by age. Let's look at how to allocate your cash for optimum growth potential and risk control.

What is Asset Allocation?

Asset allocation is the strategic distribution of an investor's portfolio across different asset classes, such as stocks, bonds, cash equivalents, and alternative investments. In simple words, asset allocation is like putting your money in different asset classes to manage risk and maximize potential returns.

The goal of asset allocation is to achieve a balance between risk and return by diversifying investments across various types of assets with different levels of risk and return potential.

Here's an example to show optimal investment allocation:

Let's consider an investor named Sarah who has $100,000 to invest. Sarah is 35 years old, has a moderate risk tolerance, and is investing for her retirement, which is still several decades away. Based on her financial goals and risk profile, Sarah decides on the following asset allocation:

Equities (Stocks): 60%

Bonds: 30%

Cash Equivalents: 10%

How to determine optimal asset allocation by age?

Your asset allocation should be purely based on your risk attitude and risk capacity. A thumb rule one could follow to begin with their asset allocation is as follows –

EQUITY ALLOCATION = 100 – Current Age

Young Investor | Mid-Age Investor | Pre-Retirees Investor | |

Age | 20 | 40 | 60 |

Formula | 100-20 | 100-40 | 100-60 |

Equity Allocation | 80 | 60 | 40 |

As you grow older, your asset allocation needs to shift from equity to debt.

What are the good parameters while selecting a good blue-chip company stock?

In this module, we will learn how to find ideal blue-chip companies. But before proceeding, let’s define Blue-chip Companies.

Blue-chip stock is the stock of a financially sound and well-established company with a large market capitalization that is a leader in its respective sector or industry. In simple terms, we can say that a blue chip company are those companies that have 3W’s

Well Established

Well Recognized

Well Financially Sound

These stocks are typically known for their stability, consistent growth, providing regular dividend payouts, and strong brand recognition. As they are less resistant to fluctuation in the economy and less volatile, these stocks are a safe choice if you’re looking to build an investment portfolio for the long term.

How to Analyze the blue-chip companies

Let’s understand what are the key parameters for analyzing blue-chip companies with a case-study of HUL (Hindustan Unilever Ltd.).

Market Capitalization: Blue-chip stocks are typically associated with large-cap companies, which have market capitalizations over Rs. 20,000 crores. Hindustan Unilever Limited (HUL) had a market capitalization of above ₹ 5,30,486 Cr.

Financial Strength: Blue-chip stocks tend to have strong balance sheets, with low debt levels relative to equity. They should also have consistent and growing revenue, earnings, and cash flow, which indicates financial stability. In FY23, HUL had a strong EBITDA was ₹14,149 cr, a 10% YoY growth.

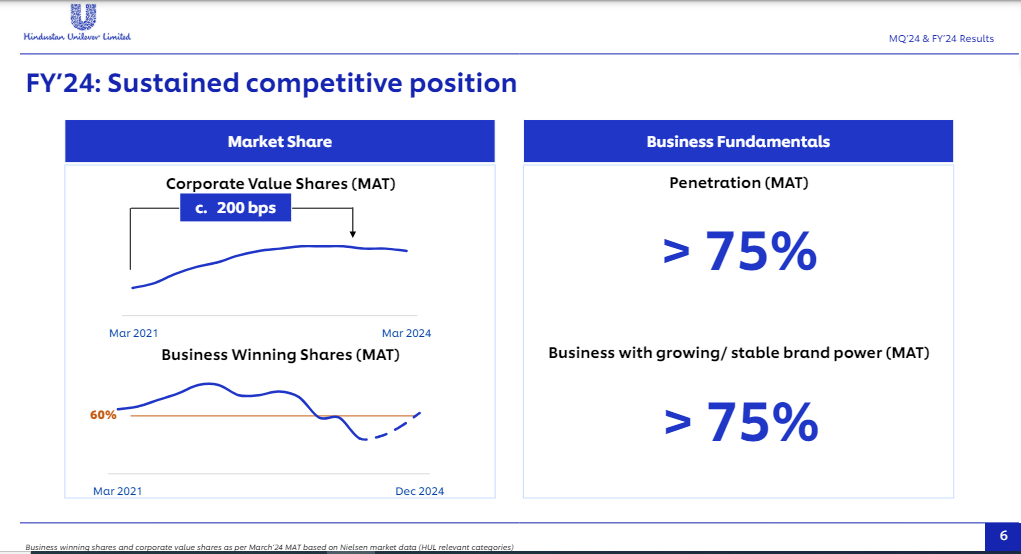

Dividend History: Many blue chip stocks have a history of paying dividends consistently and increasing them over time. Look at the below image, it clearly shows that HUL had a remarkable track of paying dividends.

Market Dominance: Blue-chip companies are often leaders in their respective industries, with strong competitive advantages such as brand recognition, economies of scale, technological innovation, or regulatory barriers to entry. Nine out of ten Indian households use HUL products across Beauty and Personal Care, Home Care, and Food and refreshment.

Global Presence: Blue chip stocks may derive a significant portion of their revenue from international markets, providing geographic diversification and exposure to global economic growth. HUL is a subsidiary of Unilever, one of the world’s leading suppliers of Food, Home Care, Personal Care and Refreshment products with sales in over 190 countries. 4% of HUL’s revenue comes from Outside India.

Track Record of Growth: While stability is important, blue chip stocks should also demonstrate a track record of consistent growth over the long term. This growth can come from expanding market share, introducing new products or services, or entering new markets. Over the years, HUL has demonstrated consistent growth through innovations, strategic acquisitions, and market expansion

Strong Management Team: Blue chip companies are typically led by experienced and competent management teams with a clear vision for the company's future growth and a commitment to creating shareholder value.

To know more check out the section on StockEdge.

How to analyse whether a new IPO will succeed or not while going forward?

In this module, you will learn how to analyse ipo stock. Initial Public Offering (IPO) is the process by which companies can go public by issuing new shares for the first time or existing shareholders sell part of their shareholding for the first time to the public.

Analyzing any listed companies and IPOs has quite the same approach. When analyzing a company, whether it's public or private, investors typically read annual reports, investor presentations, concall etc. But, when analyzing IPOs, investors face the slight challenge of limited historical data. They have only Draft Red Herring Prospectus (DRHP).

The Draft Red Herring Prospectus (DRHP) is an initial document filed with regulatory bodies by a company intending to launch an Initial Public Offering (IPO) or a public issue. It contains essential information about the company's business, operations, financial performance, and prospects.

How to Analyze an IPO

There are some factors that can impact an IPO. But before analyzing an IPO, investors should take into consideration DRPH. Let's explore how to evaluate an IPO with a case study of PAYTM (One97 Communications Ltd).

Company Background: The most important factor is to understand the business model, industry, products/services, target market, competitors, and any unique selling propositions (USPs). At that time, PAYTM had an asset-light model and earned its revenue from two innovative business models: Commerce and Cloud Services and Financial Services. As of 30 June 2021, they offered their services to 33.7 crore consumers and over 2.2 crore merchants registered with them

Sector Outlook: The sector outlook provides insights into the broader industry dynamics, including growth prospects, market trends, and regulatory factors. At that time, technology was transforming the digital scene in India, making it more accessible to both merchants and customers. The Digital India program aims to increase digital literacy, online government services, and strong digital infrastructure. Digital payments soared, reaching a market value of $20 trillion in FY21, driven by 43 billion transactions.

Objective of the IPO: When considering an IPO, it's crucial to understand its purpose. In Paytm's case, they aimed to raise Rs.18,300 crores. Of this, Rs.10,000 crores were allotted to existing investors cashing out their stake, while the remaining Rs.8300 crores were used for various purposes including marketing and promotions, customer acquisition, expanding merchant base, improving technology, and investing in new business initiatives, acquisitions, and strategic partnerships.

Risk Factors: Sector-specific risks, such as regulatory changes, industry turmoil, and cyclical downturns, can all have an impact on an IPO's prospects. In 2021, PAYTM faces challenges with net losses, increasing operating expenses, tax litigations, reliance on third-party services, negative cash flows, regulatory uncertainties, lack of dividends, rising payment processing charges, and potential harm from technology infrastructure issues.

Company’s Financial: The most crucial factor to consider when deciding whether or not to invest in an IPO is the company's financial health. At the time of the Paytm IPO, revenue from operations fell 14.6% between FY20 and FY21, but other income surged by 48.07%. Despite this, earnings increased significantly, with Rs.363 crore in FY21 compared to a loss of Rs.238 crore in FY2020.

Market Sentiments: To understand market sentiment, investors should also know its GMP (Grey Market Price). It is a premium amount paid at which initial public offering (IPO) shares are traded before they are listed on the stock exchanges. The last GMP for Paytm IPO was ₹-30. So, the expected IPO listing price as per the grey market was ₹2120, listed below the GMP price and marked as a negative listing for GMP.

Demand for the Public Issue: For any IPO, it’s important for investors to know how many investors have applied. In the case of PAYTM, it was oversubscribed 1.89 times.

Future Prospects: One of the most important factors while analyzing an IPO is the company’s plans. You should ensure that the company’s future growth prospects should be sound. At that time, the Indian FinTech industry's market size is $50 Bn in 2021 and is estimated at ~$150 Bn by 2025.

Now that you understand how to analyze an IPO, explore the upcoming IPOs that are available for subscription to determine whether they are profitable. Check out the IPO section on StockEdge.

How to calculate gains on sale of equity funds?

In this module, you will learn how to compute the gains from selling stocks. But moving forward, let’s remember the simple process of calculating the profits of the business which we have studied in class V.

Profit = Selling price – Cost Price

Right?

In the equity market, the approach is the same, but the profit is commonly referred to as capital gains. So, first understand the meaning of capital gains.

What is Capital Gain?

A capital gain is an increase in the value of an asset compared to its purchase price. In simple terms, a capital gain occurs when a share is sold at a higher price and profits are earned.

Generally, it is divided into two categories depending on the time for which the shares are held by investors.

Types of Capital Gain

Long-term Capital Gain (LTCG): Equity long term capital gain refers to the profit earned on the sale of shares held for more than one year. However, this 12 month period is valid for only listed equity shares. For unlisted shares, if the investors extend the holding period for the sale of long-term equity shares to 24 months or more, it will be considered a long-term capital gain.

Short-term Capital Gain (STCG): It refers to the profit earned on the sale of shares held for less than one year. This is valid for listed shares and in case Unlisted Equity Shares are transferred within a period of 24 months from the date of its acquisition.

Computation of Capital Gain on Equity Shares

For calculating gains on the sale of equity funds, the following formula is applicable:

Capital Gains = Asset Value (at the time of sale) - Cost of Sale (STT, brokerage, etc.) - Cost of Acquisition of the fund

Here’s the image below which shows how to calculate the net profit. Let’s break down this in a simple manner.

Let's assume that intraday equity is Short-term Capital Gain (STCG), and delivery equity is Long-term Capital Gain (LTCG).

The methods for calculating the short term & long term capital gain on equity are the same. However, the tax implications of these gains are different.

What does ownership of a company give you?

When you invest in equity shares, you become a part owner of the company.

Investing in equity shares will give you:

- Right to vote.

- Capital gains and dividends.

Tax benefits and liquidity of the money invested

How to obtain Annual Report / Quarterly report?

Yearly reports are key advertising instruments for investors that organizations put out. These reports can be obtained from the company's website.

An annual report contains few points which are:

- Address from Chairman or CEO

- Business Profile

- Financial Statements

- Management’s Analysis

What are Company Earnings and its importance for an investor?

A company’s earnings, better known as earning per share (EPS), are its after-tax overall gain, or benefits, in a given quarter or financial year. Earnings are vital while evaluating a company’s productivity and they are a central point in deciding a company’s stock cost. An investor can look at the EPS as a measure to compare companies in the same sector. Moreover, EPS forms a part for many financial ratios which help investors calculate their risk-adjusted return. A higher EPS demonstrates that the stock has a higher worth when contrasted with others in its industry.

EPS = (Net Income − Preferred Dividends)/Number of Shares Outstanding

What is Financial Planning?

Financial planning is a road-map to estimate your current and future financial position and thereby enabling you to achieve all your goals in a systematic manner.

The process of financial planning encompasses all the processes of identifying your financial goals and your risk-return needs and investing in the right products to help you achieve your goals.

Questions you should ask yourself while building a plan:

- What is my current net worth?

- What are my goals?

- How much money do I need and when?

- How much risk can I take?

- Where should I invest? - Stocks, Fixed income, Real estate, Commodity, Cash.

How do you budget? Is it necessary to have a budget?

How to budget your money?

- Determine why you need a budget: Preparing a budget is always a good decision, but it is important to define goals before starting the process.

- Try a simple budgeting plan: It is advisable that you try a plan which is simple and can be maintained by you for a long time.

- For absolute essentials, keep 50% of your income: Try to keep aside half of your income for absolute necessities in your life.

- For lifestyle expenses keep 30% of your income: Wants are those unnecessary expenses that enhance your lifestyle.

- 20% of your income should be set aside for savings: Try to keep aside 20% of your hard-earned money for savings plans, retirement corpus, debt payments and emergency funds.

Making your personalised budget is very important to build proper spending habits, keeping money aside for the long term and making sure that money is there when you actually need it.

How much emergency fund should I hold?

The exact amount of emergency fund that you should hold depends on your circumstances, but this table below gives you an idea:

- 25 Years: At this age, as you are having less liability you should be having an emergency corpus of as less as 6 months.

- 30 Years: With enhanced liabilities, your emergency corpus should be of 12 months’.

- 35 Years: You might have children and you need to have a large emergency fund to deal with medical emergencies or issues related to job loss. So, at least 18 months’ fund is required.

How much money should I save towards retirement?

It is advisable to save at least 15-25% of your income towards retirement but those who have waited long to start saving will have to contribute more.

What are goals? How can you classify your goals?

Financial goals are targets which would help to fulfill specific future financial needs.

Short term (1-3 years)

- Buying a car

- Making down payment on a home loan

- Taking vacation

- Getting married

Medium-term ( 3-7 years)

- Paying for children's education

- Home modifications

- International Travel

- Starting a new business

Long term ( more than 7 years)

- Living comfortably during retirement

- Child marriage

- Support parent's old age expenses

How to fix timelines for your goals and align them with the proper investment vehicles?

Earlier, we have discussed how to categorize our different goals as short, medium & long-term goals. Now, we will discuss several investment vehicles available according to our short, medium & long-term goals. So let's see what they are as per our investment time horizon.

Short term (1-3 years)

- Savings account

- Fixed Deposits (F.D)

- Recurring Deposits (R.D)

- Liquid Funds

- Short Term Debt Funds

- Treasury Bills

Medium-term (3-5 Years)

- Medium to long term Debt Funds

- Monthly Income Plans

- Equity Oriented Hybrid Funds

- ETFs & Index Funds

Long-term (more than 7 years)

- Large, Mid & Small-cap funds

- Equity Stocks

- Public Provident Fund (PPF)

- National Pension Scheme (NPS)

- Other long term Government bonds

How many years will it take to double your investment?

The Rule of 72 is a simple way to determine how long an investment will take to double, given a fixed annual rate of interest.

72 / Rate of Return = Time for Investment to Double

For instance, if your account earns an interest of:

6%, it will take 12 years for your cash to double (72/6 = 12)

9%, it will take 8 years for your cash to double (72/9 = 8)

12%, it will take 6 years for your cash to double (72/12 = 6)

What should you choose - Fixed Deposit OR investment in Stocks?

The decision between choosing FDs or Stocks will depend on the following factors–

Debt fund vs fixed deposit?

To answer this question, let’s discuss some basic points of differentiation between fixed deposits and debt funds–

As we can see, each instrument has their own benefits and disadvantages. Depending upon our risk appetite and return requirements, we must decide upon the type of instrument that will suit our portfolio best.

Debt fund vs Fixed Deposit

Return on Investment

Fixed Deposits (FDs) offer a fixed interest rate, which is generally lower than what you might earn from well-managed Debt Funds, especially over the long term.

Risk Assessment

FDs are very low-risk and are not affected by market fluctuations. Debt Funds, while exposed to market risks, provide stable returns and are less risky than Equity Funds. You can manage the risk in Debt Funds by diversifying and choosing funds with high-quality credit instruments.

Liquidity

FDs usually have a lock-in period and penalties for early withdrawal. Debt Funds, on the other hand, are more liquid. Investors can buy and sell them as needed without facing significant penalties.

Taxation Differences

FDs are less tax-efficient because the interest earned is taxed according to your income tax bracket. This can significantly reduce returns for those in higher tax brackets. Debt Funds offer better tax efficiency, with deferred tax treatment and indexation benefits for long-term investments.

Should I rent or buy a house?

“My Mind and Logic say - Rent a House, but my parents and my heart want me to Buy”- If this dilemma is in your mind right now, we welcome you to the adulting era.

This very debatable question- “buying vs renting home” has various reasons to support or oppose, but Indians need to make a decision that balances their Emotions and Finances.

Let’s see this with an example:

** Note: The amount saved per month and the lumpsum amount are invested in mutual funds with an expected return of 12% for next 20 years.

- Who will go for a buy?

One who wants to have an immediate sense of ownership. - Who will go for renting?

One who prefers liquidity, as this person might end up with 2.78 crores of corpus.

Financial vs Emotional Aspect

When it comes to the emotional aspects, buying a house offers a sense of accomplishment and stability. It's a significant life milestone and ensures long-term security without the worry of eviction. It also serves as a legacy to pass down through generations, albeit with societal pressures to conform. However, it can limit flexibility and entail maintenance responsibilities.

On the other hand, renting provides the freedom of flexibility, without the commitment or societal pressures, allowing for easy mobility and a sense of temporary belonging.

Financially, buying involves initial and ongoing costs, including location-based expenses and maintenance, but offers the potential for long-term value appreciation and eventual full ownership.

Renting, while simpler in terms of upfront costs and maintenance, lacks the potential for property value gain and ownership, offering instead the flexibility to adjust budgets and relocate as needed.

Buying or renting a house is very subjective to the person- Family, Income, aspirations and more. So what will you do?

Also, check out our EMI calculator

to decide better.

Can I afford to buy a house?

Are you thinking about buying a home? The first thing to consider is whether you can afford it. It's a big step, so being in a good financial spot is key. You should also consider how much you might need for a deposit, what you can borrow based on your income, and other costs when buying.

When you plan to buy a house, home affordability depends on two things:

a) Down-payment amount

b) Size of loan you can pay

Following are some assumptions based on which you can find out how much you can afford to buy a house:

Importance of Credit Score

A credit score predicts how likely you are to repay a loan on time, using info from your credit reports.

Your credit score matters a lot. It's not just about getting approved for a mortgage; it also impacts how much you pay each month. That's why boosting your credit score before applying for a mortgage is crucial. Check out some tips on improving your credit score before you go for a mortgage.

Eligibility

Before you apply for a home loan, it's important to see if you qualify. Banks and lenders look at things like your income, age, credit score, and any other debts you have. You can use a home loan eligibility calculator to figure out how much you might be able to borrow based on these factors.

What are the major points to consider while taking home loan?

If we ask you, what is that one materialistic dream you wish to fulfil right now? For the majority, the answer is- “A House”.

Buying a house is an important life goal for many of us. It's a significant investment both financially and emotionally. However, it often requires a considerable amount of money.

If you're short on cash or prefer not to dip into your investments, a home loan can be a great help. It's a type of loan you can get from a bank or housing finance company to help you buy your own home. With manageable monthly payments and the flexibility to choose your repayment period, a home loan makes it easier to turn your dream of homeownership into reality.

Major points you should know before you apply for a home loan:

Assess your home loan eligibility criteria

The different types of home loans

Various types of home loans available in India include: Regular Home Loan

Loan for Home Construction, Land or Plot Loan, Loan for Home Improvement and Extension, Top-Up Home Loan, Pre-Approved Home Loan, PMAY Loan (Pradhan Mantri Awas Yojana Loan), Balance Transfer Home Loan, NRI Home Loans

Get your home loan pre-approved

Consider these factors:

Loan amount

Cost of loan

EMI payable

Loan tenure

Documentation that needs to be submitted

For Salaried Individuals:

Identity Proof: Aadhaar Card, Passport, Voter ID, or any government-issued ID

Address Proof: Utility bills, Passport, Aadhaar Card, Voter ID

Financial Documents: Form 16, Last 3 months' Salary Slips, Last 6 months Bank Statements

Property Documents: Sale deed, Title deed, Approved building plan, Occupancy documents

Additional: Recent passport-size photographs, Completed loan application form

For Self-Employed Individuals:

Identity Proof: Aadhaar Card, Passport, Voter ID, or any government-issued ID

Address Proof: Utility bills, Passport, Aadhaar Card, Voter ID

Financial Statements: Audited financial statements of the past 2 years including Balance Sheets, Profit & Loss Statements, and ITR documents

Business Documents: GST registration, Trade license, Partnership deed, Articles of Association, SEBI registration certificate, ROC registration certificate

Bank Statements: Last 6 months Bank Statements

Additional: Recent passport-size photographs, Completed loan application form

Purchasing a loan covers a term assurance plan

Pay your EMIs regularly.

How many mutual funds should an investor have?

You must have always heard the benefits of Diversification in stocks to mitigate the risks involved. But when it comes to already diversified mutual funds,

An ideal number of mutual funds in a portfolio totally depends on a person's current income, asset allocation and risk tolerance considering the drawbacks of over-diversification.

The number of funds should be decided after asset allocation is properly determined.

The ideal number of mutual funds an investor should have is 4-5.

Beyond 5 funds, returns could be average due to the repetition of stocks in the portfolio.

These 5 funds must take care of your asset allocation

How do you decide which type of mutual fund should comprise this ideal number? For most people:

Large Cap Funds: Stick to 2 or 3 at most to avoid overlap.

Mid Cap Funds: Keep it to 2 for higher returns but higher risk.

Small Cap Funds: Limit yourself to 2 due to their high risk.

Debt Funds: 1 is ideal, but 2 is okay since they offer similar returns.

Sector Funds: Only invest if you know the industry well.

It's okay if you want to own a lot more or a lot fewer mutual funds than recommended here, as long as you make your choice based on good information.

What should be your ideal mutual fund portfolio?

Depending upon your risk appetite, there are 3 types of portfolios an investor can have–

Aggressive portfolio– suitable for people with a high-risk appetite.

An ideal portfolio may be constructed with

- 30% Large-cap stocks

- 15% Mid-cap stocks

- 15% Small-cap stocks

- 15% Intermediate-term bonds

Moderate portfolio– suitable for people with moderate to high-risk appetite.

An ideal portfolio may be constructed with:

- 40% Large-cap stocks

- 10% Small-cap stocks

- 30% Intermediate-term bonds

- 5% Cash/Money market

Conservative portfolio– suitable for people with low-risk appetite.

An ideal portfolio may be constructed with:

- 5% Large-cap stocks

- 5% Small-cap stocks

- 45% Intermediate-term bonds

- 30% Cash/Money market

What is the difference between dividend and growth options while selecting a mutual fund?

When you jump in to purchase a mutual fund, there are two options that you frequently see- Growth and Dividend. But what do they mean? Let’s discuss this in detail-

Growth vs dividend option in a mutual fund –

In dividend option plans, the dividends are distributed to the unitholders, so the NAV falls after dividends are distributed, but in the Growth option, the dividends are reinvested in the fund, so the NAV increases.

The total return in the dividend option plan is less than that in the growth plan because of periodic payouts. On the other hand, the total return of the growth option is much higher because of the long-term investment horizon.

In the dividend option plan, taxes are applicable as per the income tax slab of the investor. But in the growth option plan, the short-term & long-term gains tax depends on when you redeem your units.

Investors who need regular cash flow should go for the dividend option, but those who want to create a corpus for long-term goals should go for the growth option plan.

We hope that these key pointers have cleared all your doubts about the difference between growth and dividend funds

Which is the best mode to select in mutual funds - monthly, half-yearly or annually?

Investment in a large cap fund:

As you can see, monthly SIP gives a higher return than half-yearly or annual mode. The more times you invest, the more your money gets compounded and ensures long term benefits.

How to choose the best investment instrument for your goals?