Importance of Investments

Introduction: Importance of Investment

This module will introduce you to the importance of investments in your life. We will discuss the different types of savings and investment schemes. Additionally, we will also guide you through the various steps to get you started with your investment journey.

So, first let us understand the concept of investment in the next unit.

What is Investment?

Investing refers to the deployment of funds with the objective of earning returns either through price appreciation or passive income sources such as dividends, interest, coupon payments, etc.

It is the process of –

1.Identifying financial goals;

2.Researching the financial products available; and

3.Allocating our savings to create more wealth to achieve those goals.

Reasons for Investment:

- Realizing a return on investments

- Maintenance of a provision for future

- Fulfilling certain future objectives

- Hedge against inflation

The fundamental reason why some sort of an investment is necessary for everyone is generally to meet the "cost of inflation". Inflation is defined as a sustained increase in the prices of a basket of goods and services It is measured as an annual increase in the cost of goods and services over the previous year. An increase in inflation reduces the purchasing power of the consumer.

For instance, you could buy a box of chocolates for ₹100 five years ago. However, the same chocolates will not cost you the same as today. This is inflation at the very basic level and now we understand why we need to start investing.

The objective of investing should be to earn a return in excess of the annual inflation rate. This will ensure that we earn a return in excess of the value by which the purchasing power is eroded. Thus, people strive to achieve a return in excess of the annual inflation return which is also termed as "Real Return".

Real return is nothing but return earned after factoring in the effect of inflation and taxes so as to give a clear picture of the increase in purchasing power of an individual.

Example: If the rate of inflation is 6% p.a., then the investment should at least yield a minimum of 6% so that our purchasing power isn’t eroded.

Now that we have understood the concept of investment and its process. We will learn when and how to start an investment in our subsequent units.

When To Start?

When should one start Investing?

The sooner one starts investing the better it is because of the concept of compounding. The more time we give to our investment to grow, the more is the chance to increase wealth. Also, the fact that an investor's appetite at a young age is high and he/she can take more risks. An individual’s risk appetite is high at a young age. In case an investment decision goes wrong, there is time to work towards it and cover it up. Moreover, the financial goals, and other obligations are comparatively low in an individual’s early age.

One should choose to invest when –

1.They’re saving up for a particular financial goal, for which they will need money in later years, like retirement, child’s marriage, etc.

2.There is a fall in the interest rates offered by bank deposits and monthly savings plans.

3.They have thoroughly researched their risk and return profile, and have a clear timeline of their goals.

Factors that affect/determine your investment capability –

a)Family Information - number of earning members, number of dependent members, life expectancy

b)Personal information – age, employability, nature of job, psyche

c)Financial information – capital base, regularity of income (regular or contractual job)

d)Present worth- amount of assets already created and any liabilities undertaken like any loans

e)Past investment experience (if any)

In short, it can be said that your risk appetite determines or affects your investment profile.

Important Steps to Investing:

There are certain steps which one should always keep in mind while making an investment.

- Obtain written documents explaining the complete details of the investment

- Read and understand such documents thoroughly

- Verify the legitimacy of the investment

- Find out all the costs – direct and indirect costs to make the investment

- Assess the benefits/returns of the investment

- Be wary of the risk return profile of the investment

- Know the liquidity and safety aspects of investment

- Ascertain if the investment matches your specific financial goal

- Compare these details with other investment opportunities available in the market

- Deal only through an authorized intermediary

- Seek all clarifications about the intermediary and the investment

- Explore the other options available

(Source: NSE)

How To Start?

How to start Investing?

Most of the Investing activities are facilitated through the stock market, unlike savings which are usually done with banks. The main reason behind this is that stocks generate high returns in comparison to other asset classes. Compared to simple savings in a bank account, the process of investing is little more elaborate, but with the right knowledge, one can easily learn how to invest in the stock market.Investing for a novice should essentially begin with the identification of his/her short, medium and long-term goals. It is very crucial to understand how much risk an individual can take. Risk is essentially the amount of money one can afford to lose, if an investment ends up making losses. It is also known as an investor’s risk appetite.As per their risk appetite, beginners need to conduct an analysis of what kind of financial products suit both their goals as well as the risk appetite.

Getting back to stocks, they can do this with the help of two broad analysis techniques –

1.Fundamental Analysis: The process of analysing the financial status of a company and the industry in which it is operating to make an investing or trading decision.

2.Technical Analysis: The process of analysing charts with the help of patterns and indicators, to identify possible price trends in the future.

Beginners can choose either one of these, or a combination of both these techniques, to filter out the best potential investments from the stock market. However, it is always preferred to use a combination of both Fundamental and Technical analysis to get the high probability return generating investment ideas. Apart from this, there are some other concerns that need to be addressed while investing. We will discuss them in the next unit.

Concerns While Investing

What are the investment concerns that need to be addressed, while investing and choosing the assets?

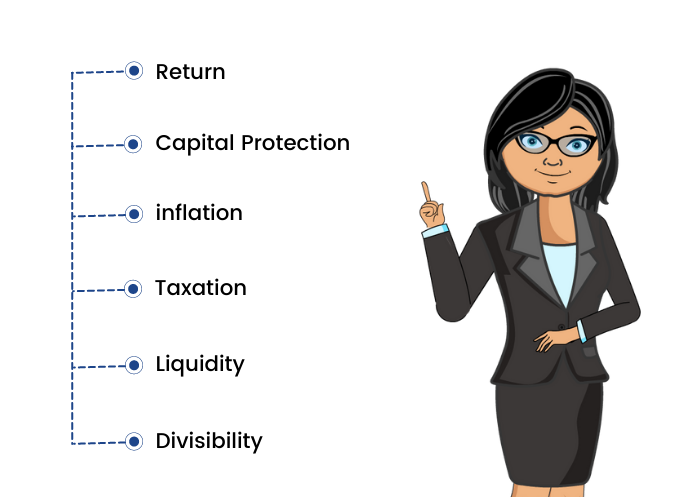

The most common concerns that needs to be addressed, while investing and choosing the assets are-

Returns

The return from the investment could be in the form of capital gains, interim cash flows, or both. A retired person might be needing regular cash flows to meet daily expenses, whereas a younger person in the working or accumulation phase might be more concerned with growth of his investment to create a corpus for his retirement.

Capital Protection

The most important aspect of investment is to protect capital. Investors are generally deemed to be risk averse. We feel investments are risky and thus leave most of our saved money in instruments earning low income, without understanding the effect of inflation, which reduces the value of our money every day.

Risk is a part of our lives. There is risk associated with anything or everything we do. Even if we cross a road, there is a risk of meeting with an accident. Risk and reward go hand in hand, higher the risk, higher is the reward expected.

Each of the investment assets has its own associated risk and reward return, which one must understand before investing his money in any of the investment vehicles.

Inflation

By definition, inflation is the sustained rise in the general level of prices of goods and services in an economy over a period of time. When prices rise, each unit of currency buys fewer goods and services, resulting in erosion in the purchasing power of money. The aim of investment is to get returns in order to increase the real value of the money. In other words, your investment should be able to beat inflation.

Taxation

Income from our investment assets is liable to taxation, which is going to reduce our returns. You should remember that the real return (read positive return) from any investment product would be the return after accounting for taxation and inflation.

Liquidity

It is the ability to convert an investment into cash quickly, without the loss of a significant amount of the value of the investment. If you would need a particular amount at a short notice then invest in an investment product with high liquidity.

Divisibility

This is the ability to convert part of the investment asset into cash, without liquidating the whole of the asset. Divisibility may be an important consideration for many investors, while choosing an investment vehicle. For example, while investing ₹15,00,000 in a senior citizen scheme, one could increase the divisibility without affecting returns by dividing this investment into smaller ticket sizes of say ₹3,00,000 , rather than investing the entire amount in one go.

Before committing your capital to any investment vehicle, it is preferable to consider your financial needs, goals, and aspirations, as well as the risk profile.

But first, let us discuss a few pros and cons of investment in the next unit.

Pros & Cons of Investments

What are the benefits and disbenefits associated with investments?

Pros:

1. Investing helps us beat inflationary pressure. In fact, investing in the equity segment can often make money grow at a rate which beats inflation in the future.

2. Investing beats inflation with a unique feature known as the compounding of wealth. Simply put, the earlier we invest, the more our earnings will multiply with the passage of time.

3. It is because of the power of compounding that we do fulfill our goals by sacrificing little amounts of money over a long period of time.

Cons:

1. Investing requires domain knowledge, along with some basic analytical skills, and emotional intelligence. It takes intensive practice to become a skilful investor.

2. Investments are affected by a wide range of factors like economical events, company results, etc. One has to study all the relevant factors to be successful.

3. Investing returns come at the cost of proportionate risks. Returns are never guaranteed in any form of investing.

Note: Till now, in this module, we have covered the basics of investment and also the pros and cons of investment. But what are different investment avenues available? Let us discuss them in the next unit.

Avenues of Investments

What are the various avenues of investments?

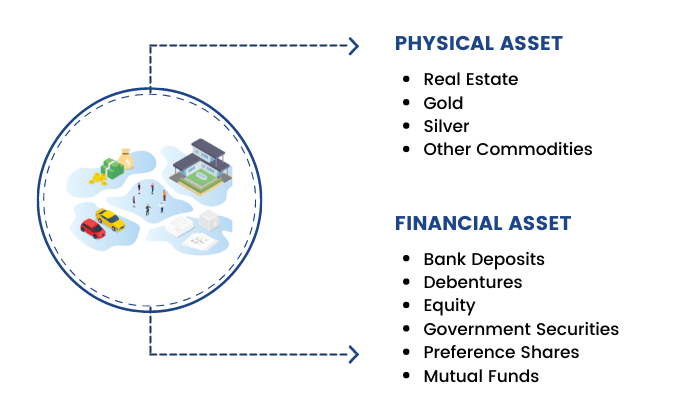

The avenues of investments can be broadly classified into two categories: Physical Assets and Financial Assets.

- Physical Assets are tangible, material assets such as Real Estate, Gold, Precious Stones, Antiques, Commodities, etc. The return on investments in physical assets can be earned when the assets are sold. Hence, the return is earned in the form of capital gains (appreciation).

- Financial Assets are intangible assets, the value of which is derived from the contractual agreement. Examples of Financial Assets – Bank Deposits, Debentures, Equity, Government Securities, Preference Shares, Mutual Funds, etc. The return on investments in financial assets can be divided in two parts – interim cash flows (interest, dividend, etc.) & Capital Appreciation

Financial Assets can be further classified as –

1) Assets with fixed returns –

The returns associated with such investments are fixed i.e. they either provide a stable rate of interest or dividends to the investors. Apart from earning fixed return, an investor can also trade these assets to earn capital gains. Examples – Debentures, Preference Shares, Public Sector Bonds, Government Securities.

2) Assets with variable returns –

The returns associated with such investments varies from time to time. Usually, investors expect higher returns from such assets as compensation for higher risk involved. Examples – Equity Shares, Mutual Funds, etc.

The market is flooded with different modes of investment. However, it depends on the risk aversion ability of the investor as to whether he invests in high-risk options with greater returns, low risk options with moderate returns or risk-free avenues. But before we start with our investment journey, there are some fundamental rules of investing. We will learn this in our next unit.

Fundamental Rules of Investing

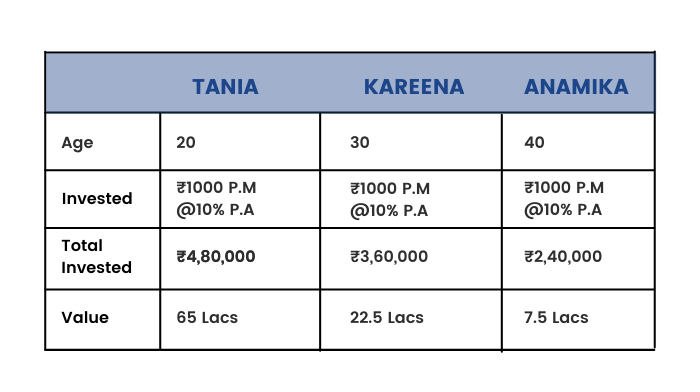

There are three fundamental rules of investments:

Example - Raj started investing money to the tune of ₹5,000 per month diligently. He began this discipline at the age of 22. He was earning a rate of interest of 12% compounded each year. While his friend, Amrita started investing money to the tune of ₹10,000 per month. She was also doing this very religiously. She also earned 12% compounded. She started the process of doing the investments month on month, at the age of 30. What is the total investment adding up to at the age of 50 years of age?

Therefore, it is very important to start investing early. The earlier, the better for your investments. But before you start investing your money, you need to save a portion of your income that can be used to make investments. So we will discuss the concept of savings, also its pros and cons in the subsequent units. As you can see from the table the cost of waiting / delaying for Amrita is ₹37,63,806. Raj benefited from eight more years of compounded growth than Amrita.

Savings

What is Saving?

Savings include the money that is left after one deducts their expenditures from their income.

To put it simply,

Savings = Income – Expenditure.

Saving money is the first step towards financial security. When someone saves money, they can use it to –

1.Protect themselves from emergencies;

2.Build a corpus of funds for retirement; or

3.Invest and make it grow more.

How to start Saving?

Savings are usually maintained with the usage of bank facilities like savings accounts and fixed deposits.

Apart from these, one can choose from a variety of periodical yearly and monthly savings plans like –

1.Post Office Monthly Income Schemes (MIS)

3.Sukanya Samriddhi Yojana (SSY)

However, sometimes it can be hard to save money due to an influx of expenses that go unrecorded.

Therefore, one needs to set out a clear strategy to save regularly and efficiently.

The best way to do so is to start budgeting.

A budget is a plan-of-action that lays down income allocations towards various expenses and helps us limit our spending on unnecessary expenses.

If one is unsure about the limits we should be setting upon our spending and savings, we can use thumb rules like the 50-30-20 rule to start budgeting.

Click Here to know the details about the 50-30-20 Rule.

Later, this rule can be tweaked as per one’s needs and goals.

Pros And Cons of Savings

What are the Pros and Cons of Savings?

Pros:

1.Savings remain unaffected by any events of the economy. Since they don’t fluctuate in value, we can reach our goals as per a set timeline and a fixed amount.

2.Savings form the fundamental step of investment. If you don’t save, you won’t have anything to invest.

3.Savings can help us save for goals in the most disciplined manner.

Cons:

1.Due to inflation, the purchasing power of our money can fall over time. Therefore, saving is most suitable for short-term goals only.

2.Most savings plans do offer interest rates, but these aren’t high enough to counter the effect of inflation.

3.You have to save a large corpus of money to reach big goals, as your money will not be growing over time.

When should you save?

The pros and cons that we read above show that there are only specific circumstances under which saving money can be useful.

One should, therefore, save their money when –

1.They are saving up for a short-term goal which doesn’t require a large amount of money, like a vacation, etc.

2.They are building an emergency fund, or saving up for retirement.

3.They don’t have any urgent debt obligations.

4.They want to invest in the near future.

Saving And Investment Schemes

Earlier in this module, we learned about savings and investments. We have also discussed the pros and cons for each of them. In this unit, let us discuss a few savings and investments schemes available to us.

What are various Long-term and Short-term Saving Schemes?

- Kisan Vikash Patra: A savings scheme that is available at all Head Post Offices and Authorized Post Offices throughout India. Investments in KVP can be in denominations of ₹1,000. Any savings in the KVP will double the amount invested in 10 years and 4 months. The Interest rate offered is 6.90% (As of June, 2021) per annum compounded annually. Premature encashment is available only at a discount. However, this instrument offers no tax savings like the PPF and NSC.

- Public Provident Fund: A savings instrument with a long-term horizon having a maturity period of 15 years and an interest rate of 7.10% compounded annually (As of Q1 2021-22). A PPF account can be opened through a nationalized bank anytime during a year and is open all through the year for depositing the money. There is a tax benefit available on the amount invested and also the interest that gets accrued every year. A withdrawal is permissible every year from the seventh financial year of the date of opening the account and the amount of withdrawal will be limited to 50 percent of the balance at credit at the end of 4th year immediately preceding the year in which the amount is withdrawn or at the end of the preceding year whichever is lower. However, with the recent changes in PPF rules, one can prematurely close his PPF account after completion of 5 years of opening the account but, premature closure is allowed only under specified conditions.

- Company Fixed Deposits: These are short term (6 months) to medium term (3-5 years) borrowings by companies at a fixed rate of interest which is payable monthly, quarterly, semiannually or annually. They can also be cumulative fixed deposits where the entire principal along with the interest is paid at the end of the loan period. The rate of interest varies between 6-10% per annum for company FD's. The interest is received after deduction of tax.

- National Savings Certificate (NSC's): These are issued by the Department of Post, Government of India and are available at all post offices in the country.

The minimum amount that can be invested is INR 100, and in multiples thereof. There is no upper limit for investment in this scheme. Certificates are issued in the denomination of ₹100 for a maturity period of 5 years. The certificates are also transferable. The interest rate offered is 6.80% compounded annually which the government revises every quarter. The interest that is earned through NSC is taxable under the slab ‘Income from other sources. The interest that is earned each year in the scheme is reinvested every year. The amount that is re-invested each year attracts tax benefits under Section 80C. Since the maturity period of NSC is five years, the interest can be re-invested for only four years. The interest earned in the fifth year is paid to the investor with the maturity amount. So, the tax benefit can be availed only for the first four years of the investment period. The interest earned in the final year is taxable.

- Bonds: It is a fixed income instrument issued with the intent of raising capital through debt. The Government and Financial Institutions alike sell bonds. A bond is defined as a promise to pay back the principal along with a fixed rate of coupon payments on a specified date mentioned in the bond itself.

- Mutual Funds: A mutual fund is a professionally managed fund that creates a pool of capital by raising money from the public and invests in a group of assets (stocks, bonds, money market instruments, etc). It is a proxy to investment for people who have no knowledge of how the financial system operates and want a professional to manage their money on their behalf. Investment in mutual funds is done through units which are calculated based on the Net Asset Value (NAV) of the fund which is determined at the end of every trading session. Mutual funds are of two categories viz open ended and closed end mutual funds. Investment can be done for a specified horizon based on the investor’s needs.

- Equity/Share: The paid-up equity capital of a company is divided into equal units of small denominations; each called a share. For example, in a company, the total equity capital of Rs 2 crore is divided into 20 lakh units of Rs 10 each. Each such unit is called a share. Thus, the company then is said to have 20 lakh shares of Rs 10 each. The holders of these shares are owners of the company and have voting rights.

- Debt Instrument: It represents a contract wherein one party lends money to another on a pre-determined basis with regards to rate and periodicity of interest, repayment of principal amount by borrower to the lender. In the Indian Securities market, the use of debt instruments issued by Central & State Governments and public sector organizations and the term 'debenture' is used for instruments issued by corporate sector.

- Derivatives: Derivative is a product where in a contract is made based on the value of an underlying asset. It is not something tangible but just a contract. It is a financial contract where the value of the contract is interlinked with the future price movements of the underlying asset. The underlying asset can be equity, commodity, index, bond or any other asset.

Derivatives were initially introduced as hedging devices and to protect against the fluctuation in spot prices in the market but since then have gained popularity among market participants.

The interest rates of all small saving schemes (post office schemes) like NSC, PPF and KVP are reset on a quarterly basis by the Government of India.

Saving Or Investing

Now that you are familiar with several savings and investment schemes, you must be wondering, Which is best for you, Saving or Investing? – Which one is ideal for a beginner?

The following essential differences can be pointed out between saving and investing –

1. Meaning:

While savings refer to simply setting aside money for a goal, investment is the process of buying assets with these savings to grow our wealth.

2. Purpose:

Savings are mostly done for achieving short term goals, while some medium-term goals can be achieved through bank deposits as well. Investments, on the other hand, are needed to achieve long-term goals, which have to be reached at least ten years from now.

3. Risk:

Savings pose minimal risk, whereas when it comes to investing, one can find products offering products to suit different risk appetites.

4. Products:

Savings is usually carried out through bank accounts and deposits, and government saving schemes.

Click here to know more about Government Saving Schemes

Investing is carried out through the various segments of the stock market, namely, equity, debt, and derivatives.

How to decide whether you should Save or Invest?

It can be deduced that long-term goals should be backed up by investments and short-term goals should be achieved through savings. Thus, one way of deciding whether we should save or invest in the type of goal we are setting money aside for. Another factor affecting this decision is your financial situation.

Here, some elements of financial security, like an emergency fund, require savings first.

Click Here to know more about of financial security, like an emergency fund.

Also, if you are currently having some debt obligations at hand, you should focus on saving the required amount, and use it to pay off your debt. However, in the absence of debt, you can concentrate your savings towards investing dedicatedly. Lastly, another factor affecting this decision is the rate of return you are looking for. If you are relying on higher returns on a sum of money to bring you closer to your goals, you need to invest your money. If not, savings products are adequate for you.

Should you Save and Invest together as a beginner?

An important point to note here is that, for a beginner, saving should always come before investing, and never together. Why?

Firstly, how will we invest, if we don’t save any money for it? Also, a beginner to saving and investing will be someone who has just started earning money. At such a position, one needs to ensure that they first have their financial goals and priorities laid out for them.

While they figure out their goals, they should build the habit of disciplined saving. Once the discipline is built, a beginner will find it easier to build the habit of investing in the near future as well. Therefore, as a beginner, save first, build the required discipline and funds needed to invest, then invest. As we saw through this writeup, we can come to the conclusion that both saving and investing are fundamental steps to ensure that we can be as financially secure as possible. While saving builds discipline, investing helps us grow our wealth, provided that we know how to invest in the stock market.

Click here to know more about How to invest in stock markets.

Interest Rates

Earlier in this module, we encountered the word "Interest" several times. So, in this unit, let us elaborate on the concept of interest and interest rates.

What is Interest and Interest Rates? What are the factors that govern interest rates in an economy?

Interest

Interest is the amount charged to the borrower for the privilege of using the lender's money. It is calculated as a percentage of the principal balance (the amount borrowed). There are two methods to calculate interest- simple interest and compound interest. We will learn both of them in the upcoming units of this module.

Interest Rates

It is the rate at which the borrower pays interest on a loan. Interest rates have a bearing on all fixed income securities and other Government instruments as well because the price of all these securities have an inverse relation with interest rates.

The factors which govern these interest rates are mostly related to the overall economic structure and are referred to as macroeconomic factors which can be summarized as:

- Budgetary Deficit: Budget deficit occurs when the spending of the government exceeds its income over a given period.

- Supply & Demand of Money: The supply and demand of money influences the monetary decisions by the RBI. When the RBI feels that liquidity is plenty in the economy and spending should be curtailed to avoid overheating of the economy, it decreases the supply of money and when it feels that economic growth is slowing down and liquidity is scarce, it increases the supply of money.

- Inflation rate: Inflation is the persistent increase in the price levels of a particular commodity over a period of time. The key word here is persistent because inflation occurs only when prices keep increasing on a constant basis.

Inflation can be of two types, cost push and demand-pull inflation wherein cost push means when there is a gradual increase in cost of raw materials which in turn leads to an increase in the prices of the goods while demand pull inflation is a case where the demand increases at a rate faster than the supply which leads to an increase in the prices.

Let us also consider two other probable scenarios:

To cool down high inflation: the interest rate is increased.

When the interest rate rises, the cost of borrowing rises. This makes borrowing expensive. Hence borrowing will decline and as such the money supply (i.e. the amount of money in circulation) will fall. A fall in the money supply will lead to people having less money to spend on goods and services. Hence, they will buy a lesser amount of goods and services. This, in turn, will lead to a fall in the demand for goods and services. With the supply remaining constant and the demand for goods and services declining; the price of goods and services will fall. As inflation is a continuous increase in the general price level of goods and services so a fall in the general price level of goods and services will lead to a decline in inflation levels.

In low inflationary situations, the interest rate is reduced

A fall in interest rates will make borrowing cheaper. Hence, borrowing will increase and the money supply will also increase. With a rise in money supply, people will have more money to spend on goods and services. So, the demand for goods and services will increase and with supply remaining constant this leads to a rise in the price level i.e. inflation.

Risk Free Interest Rate

In this section, let us discuss another concept related to interest rates called "Risk Free Interest Rate''.

What do you understand about the Risk Free Interest Rate?

The real risk-free rate of interest is a theoretical rate on a single period loan that has no expectation of inflation in it. Real rate of return is also known as an investor's increase in purchasing power (after adjusting for inflation). Since expected inflation in future periods is not zero, the rates we observe on G-Sec, for example, are risk-free rates but not real rates of return. G-Sec rates are nominal risk-free rates because they contain an inflation premium.

Nominal risk-free rate = real risk-free rate + expected inflation rate

Equilibrium interest rates are the required rate of return for a particular investment, in the sense that the market rate of return is the return that investors and savers require to get them to willingly lend their funds.

Interest rates, also referred to as discount rates, and the terms are often used interchangeably. If an individual can borrow funds at an interest rate of 20%, then that individual should discount payments to be made in the future at that rate in order to get their equivalent value in money. Interest rates can also be viewed as the opportunity cost of current consumption. If the market rate of interest on one-year securities is 7%, earning an additional 7% is the opportunity forgone when current consumption is chosen rather than saving (postponing consumption).

Simple Interest Vs Compound Interest

Concept of Simple Interest

Simple Interest is the interest paid only on the principal amount borrowed. No interest is paid on the interest accrued during the term of the loan.

There are three components to calculate simple interest: principal, interest rate and time.

Formula for Calculating Simple Interest

Interest = P x R x T

- I = Interest

- P = Principal

- R = Interest rate

- T = Time

Example: Mr. X borrowed ₹10,000 from a bank to purchase a household item. He agreed to repay the amount in 8 months, plus simple interest at an interest rate of 10% per annum. If he repays the full amount of ₹10,000 in eight months, the interest would be:

P = ₹10,000; r = .10, t = 8/12

Applying the above formula, interest would be:

I= ₹10,000*(.10) *(8/12) = ₹667

This is the simple interest on the loan of ₹10,000 loan taken by Mr. X for 8 months.

If he repays the amount of ₹10,000 in fifteen months, the only change is w.r.t. time.

Therefore, his interest would be:

I = ₹10,000*(0.1) *15/12 = ₹1,250

Compound Interest

Compound Interest is the interest on a loan calculated on both the principal borrowed and interest earned. Interest is paid on the interest already earned.

Formula for Calculating Compound Interest

Amount = Principal x (1+interest rate) ^ (time)

Compound Interest earned = Amount – Principal = P{(1+r) ^ t-1}

Where,

- P = Principal

- r = Compound Interest Rate

- t = Time

Example: Mr. A borrowed ₹1,00,000 from a bank for his daughter’s education. He agreed to repay the amount in 2 years with an interest rate of 12% compounded annually. What is the interest paid by Mr. A?

After 2 years, Mr. A paid = 1,00,000*(1.12) ^2 = ₹1,25,440

Compound Interest = 1,25,440 - 1,00,0000 = ₹25,440

Albert Einstein once described compound interest as the “eighth wonder of the world,” let us discuss more on this in our next unit.

The Power of Compounding

“The big money is not in the buying and selling but in the waiting “ - Charlie Munger, Berkshire Hathaway

In the investing circuit, compounding is often regarded as the eighth wonder of the world. We will always keep coming back to the advantage of yours over everyone else while discussing this lesson. Compounded Growth is the reason why most people choose to save in the first place. The Compounding effect is perhaps the strongest force out there that will propel you to start saving and growing your wealth at the earliest. The power of compounding can grow your wealth exponentially.

Let us assume Mr.X holds a Fixed Deposit worth ₹10,000 for a tenure of 365 days at an interest rate of 10% p.a.

A year later, he is eligible to receive ₹11,000 ( ₹10,000*110%)

His annual interest income = ₹11,000 -₹10,000 = ₹1,000

But instead of withdrawing his investment, what if he chose to stay invested for a longer period of time.

This time, Mr.X will receive 10% on the new principal amount i.e. ₹11,000

Hence his annual interest income will be ₹1,100 (10% of ₹11,000)

Did you notice the difference?

Just by staying invested for one extra year, Mr.X earned an extra ₹100 of interest. Although, this ₹100 may sound extremely frugal at the moment but it makes a big big difference when you are invested for the long term.

Here’s how,

Let us assume a hypothetical scenario- Mr.X and Mr.Y have an initial capital of ₹1,00,000 and are scouting for potential opportunities for investment. Both have the same time horizon i.e. 20 years and decide to invest in Fixed Deposits at an interest rate of 8% p.a. Mr.X decides to reinvest his profits whereas Mr.Y withdraws them at the end of every financial year.

At the end of 20 years,

Just by reinvesting a small portion of the interest, Mr.X was able to save a substantially higher amount at the end. Now, work out the math for the compounding effect if the principal would have been higher, say ₹10 lakh or ₹1 crore.

Let us do it again,

The more the principal amount, the higher is the compound effect.

Let us bring another factor into consideration, our favorite one-time.

If Mr.X had invested the exact same amount for a shorter duration say ten years, you would expect the amount of maturity to be exactly half that of the twenty year maturity i.e.

Amount at the end of ten years = 50% * ₹46,60,957 = ₹23,30,454

Let us check for the validity of this thesis,

The amount at the end of ten years = ₹21.58,925

This corresponds to a difference of ₹1,71,529. Huge indeed!

Note- We have already solved the math for you to simplify things. You can calculate CAGR (Compounded Annual Growth Rate) using various online tools.

Simply put,

An initial capital of ₹10,00,000, invested @8% p.a. over twenty years grows to:

Hence proved, the higher the principal and duration invested, the higher is the compounding effect.

Also, keep in mind that we have assumed meagre returns of 8% p.a for conservative investors. The actual return on stocks is much higher. Let us see how much ₹1,00,000 invested in a few large cap stocks exactly ten years ago have fared,

Now, that's impressive!

Conclusion

We have summarized the key takeaways from this module:

- Start as early as Possible - Don’t delay your first investment, Start Now!

- No amount is too small - It is the little drops of water than make a mighty ocean

- Adopt the mentality of wise men - Income - Savings = Expenditure

- Do not keep your savings in the form of idle cash

- Set the primary target of beating the inflation rate

- Traditional method of savings such as Bank FDs and PPF accounts will not fulfill your objective

- Ideally, you should divide your corpus between Equity & other investments ( Gold, Bank FDs, Bonds) in the following manner:

100-Age = Equity Percentage Allocation

- Wealth accumulation is a slow and steady process.

- Set Reasonable risk-return expectations

- Equity is the best performing asset class

- Stocks are in a long-term uptrend.

- Volatility is a boon and we can make it work to our favour.

- Large cap companies have an established track record and are best suited for investors with low risk-appetite.

- Midcap & Smallcap stocks have delivered better returns than their largecap peers but carry higher risk.

- Patience is a gifted virtue and more so for long-term investors.

- Investors must not panic when the market falls but instead add to their positions if they are confident about the prospects of the company.

- Returns are quadrupled when stocks are bought on market declines

- Investors who do not have time to track the markets can seek professional management of their funds and invest via the Mutual Fund (SIP Route) or ETFs

- The StockEdge App is a must have tool for DIY investors

- You can browse through our other modules at ELM School to enlighten yourself about the financial jungle. Start with this.

- Stay invested for the long-haul and enjoy the magic of compounding.